Maria Shepherd, President and Founder, Medi-Vantage11.04.20

When the first reports were issued about paclitaxel, many were concerned about paclitaxel coated stents and possible increased mortality in patients treated with paclitaxel-coated stents/balloons for peripheral artery disease.1 The authors of a JACC article cite multiple meta-analyses as do those who argue against the use of paclitaxel coated devices, but the real question is, what impact does this have on interventional cardiology devices?

In 1993, the FDA approved the first coronary intervention stent in the U.S., Cook Medical’s Gianturco-Roubin Flex Stent bare-metal stent (BMS). Approval of the Flex-Stent came one year after a review by FDA’s circulatory system devices panel.2

Cook launched its coronary stent with great fanfare using company-sponsored training sessions beginning in July 1993 and priced it at $1,150.2 Interventional cardiologists (IC) were enthusiastic about the potential for the stent technology to treat coronary artery disease and lined up for training to treat their patients. The stent was also marketed in Korea, Australia, and Singapore.

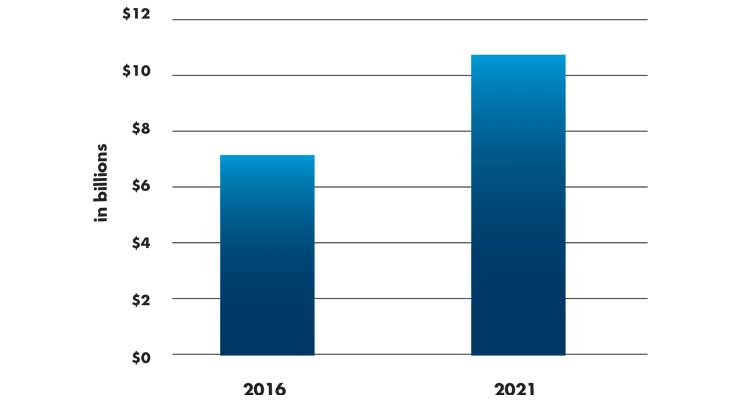

With such an enormous lead, how did Cook lose first-mover advantage in a market that would grow to more than $7 billion in global sales? The coronary stent market is forecasted to grow from $7.16 billion in 2016 and reach $10.3 billion by 2021 (Table 1) with an astonishing CAGR of 7.6 percent in a market almost 30 years old.3

Table 1: Global stent market growth3

Why Is It Important?

At the time, before the market direction was clear, game changing product design decisions like “Which drug coating do we use on our first DES?” are incredibly tough calls to make—significant dollars and market position are at risk.

It began with the introduction of higher cost drug-eluting stents (DES) that caused a significant shift in the revenues of the stent market. DES were first sold in the U.S. in 2002, a daring strategic move with higher business risk to cardiovascular device companies, but it also offered the upside of delivering the holy grail—a lower restenosis rate. Choosing the drug to use to coat the BMS was a complex decision for companies. Many pharmaceutical compounds were evaluated, including Taxol (paclitaxel), which was also used as an anti-cancer medication. It was argued paclitaxel was a risk to patient safety because the dosage range over which paclitaxel is used in stenting is close to the drug’s toxicity level.4

Cordis (then a division of Johnson & Johnson; now part of Cardinal Health) chose Sirolimus in its DES and began an exclusive licensing agreement with Wyeth Pharmaceuticals. Cordis chose Sirolimus because it could inhibit cellular growth linked to restenosis, could be formulated into a polymer matrix, and was highly stable. Sirolimus is effective over a wide range of concentrations and, in evaluations, was non-toxic at high concentrations. The Cordis Cypher was the first mover in the DES market.

By 2003, the Cypher penetrated the BMS market by more than 60 percent. Cordis had many competitors—Boston Scientific, Guidant, and Medtronic—all working on DES offerings. In 2004, Boston Scientific was awarded FDA approval for its Taxus DES.

Newcomers to this competitive market know clinical data is a must have, and industry relationships are hard to displace. Almost all ICs take charge in the interventional suite and medical device representatives have their work cut out for them to be subtly central to the procedure to generate and maintain influence, while bringing service to the IC that cultivates loyalty to the products, the sales person, and the company.5 Medtech representatives and some doctors think a sales rep brings many benefits to the hospital, by amplifying productivity and offsetting deficits of procedure room staff.

Where Is This Growth Coming From?

Of the three major segments of coronary stents—BMS, DES, and bioabsorbable stents—bioabsorbable stents are expected to have the highest growth between now and 2022,6 although they represent the smallest revenue segment of the group. The worldwide bioabsorbable stent market is forecast to reach $417 million by 2022, up from $242 million in 2017 (Table 2)—a CAGR of 11.5 percent.6 Market drivers of bioresorbable stents are the growing aging population, rising percutaneous coronary intervention procedures, and increasing demand created by medical device manufacturers’ clinical trials of bioresorbable stents. There are highly regarded clinical benefits attributed to bioresorbable stents, such as a decrease in thrombosis and inflammation complications.7 One market obstacle was the high cost of bioabsorbable coronary stents when the Absorb stent from Abbott was introduced in 2016.

Table 2: Global bioabsorbable stent market revenue forecast6

Shifting the ASP Up, Up, Up

It doesn’t happen very often, but when introduced, the innovation and promise of bioabsorbable coronary stents caused an ASP shift in the upwards direction. ASP data is difficult to obtain and a 2019 article about the sales of coronary stents in India provide insights to global pricing and the power of enormous market demand in a country with a population of more than 1.4 billion people.

In February 2017, the government of India regulated the selling price of coronary stents. According to an interventional cardiologist in India, stent prices dropped by an average of 80 percent.8

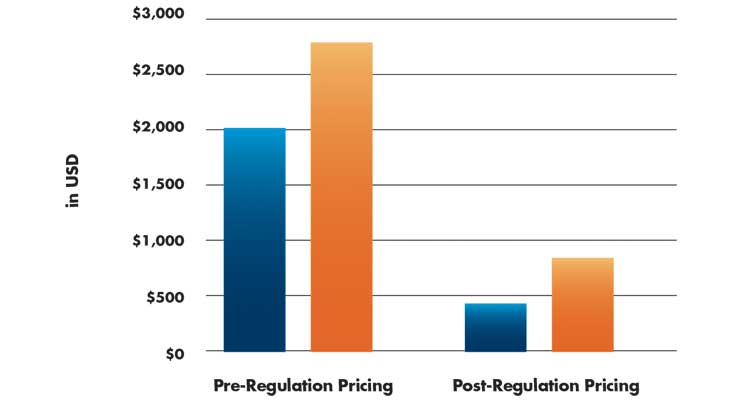

Before the price was regulated, the cost to the patient of the only approved bioresorbable stent in India was 200,000 Indian Rupees (INR; approximately $2,800), compared to DES costs that ranged from INR 85,000 to 160,000 ($1,190 to $2,240). Allegations were made that hospitals and ICs obtained kickbacks for implanting stents.8

The Indian government cut and regulated stent prices significantly (Table 3). The cost for patients for a bioabsorbable stent was stabilized to INR 60,000 (approximately $840). BMS and DES were capped at INR 7,500 and 30,000, respectively ($105 and $420).8 The government reportedly used industry-supplied data while Indian physicians voiced concerns about how low profitability would drive away large stent manufacturers from supplying the newest technologies. The medical device industry pushed back, stating that supplying cardiology products at a loss would cause them to lose money, obviously to put pressure on the government. In early 2017, Abbott announced it would withdraw two stents from the Indian market after the government’s move to cap stent prices.9 The Abbott bioresorbable stent disappeared from shelves.

Table 3: Changes to stent prices in India (2017)8

The Medi-Vantage Perspective

By 2020, DES continued to dominate the overall coronary stent market and had the highest revenue market share forecasted until the end of 2024, estimated at nearly 95 percent of the total market.10 Good marketing and an intimate knowledge of pricing strategy was central to managing this enormous global market. Make price strategy a key part of your marketing and product development so the market you manage gets all the investment in development it warrants at your medical device company.

References

Maria Shepherd has more than 20 years of leadership experience in medical device/life-science marketing in small startups and top-tier companies. After her industry career, including her role as VP of marketing for Oridion Medical where she boosted the company valuation prior to its acquisition by Medtronic, and director of marketing for Philips Medical, she founded Medi-Vantage. Medi-Vantage provides marketing and business strategy and innovation research for the medical device industry. Shepherd has taught marketing and product development courses, speaks regularly at medtech conferences, and can be reached at mshepherd@medi-vantage. Visit her website at www.medi-vantage.com.

In 1993, the FDA approved the first coronary intervention stent in the U.S., Cook Medical’s Gianturco-Roubin Flex Stent bare-metal stent (BMS). Approval of the Flex-Stent came one year after a review by FDA’s circulatory system devices panel.2

Cook launched its coronary stent with great fanfare using company-sponsored training sessions beginning in July 1993 and priced it at $1,150.2 Interventional cardiologists (IC) were enthusiastic about the potential for the stent technology to treat coronary artery disease and lined up for training to treat their patients. The stent was also marketed in Korea, Australia, and Singapore.

With such an enormous lead, how did Cook lose first-mover advantage in a market that would grow to more than $7 billion in global sales? The coronary stent market is forecasted to grow from $7.16 billion in 2016 and reach $10.3 billion by 2021 (Table 1) with an astonishing CAGR of 7.6 percent in a market almost 30 years old.3

Table 1: Global stent market growth3

Why Is It Important?

At the time, before the market direction was clear, game changing product design decisions like “Which drug coating do we use on our first DES?” are incredibly tough calls to make—significant dollars and market position are at risk.

It began with the introduction of higher cost drug-eluting stents (DES) that caused a significant shift in the revenues of the stent market. DES were first sold in the U.S. in 2002, a daring strategic move with higher business risk to cardiovascular device companies, but it also offered the upside of delivering the holy grail—a lower restenosis rate. Choosing the drug to use to coat the BMS was a complex decision for companies. Many pharmaceutical compounds were evaluated, including Taxol (paclitaxel), which was also used as an anti-cancer medication. It was argued paclitaxel was a risk to patient safety because the dosage range over which paclitaxel is used in stenting is close to the drug’s toxicity level.4

Cordis (then a division of Johnson & Johnson; now part of Cardinal Health) chose Sirolimus in its DES and began an exclusive licensing agreement with Wyeth Pharmaceuticals. Cordis chose Sirolimus because it could inhibit cellular growth linked to restenosis, could be formulated into a polymer matrix, and was highly stable. Sirolimus is effective over a wide range of concentrations and, in evaluations, was non-toxic at high concentrations. The Cordis Cypher was the first mover in the DES market.

By 2003, the Cypher penetrated the BMS market by more than 60 percent. Cordis had many competitors—Boston Scientific, Guidant, and Medtronic—all working on DES offerings. In 2004, Boston Scientific was awarded FDA approval for its Taxus DES.

Newcomers to this competitive market know clinical data is a must have, and industry relationships are hard to displace. Almost all ICs take charge in the interventional suite and medical device representatives have their work cut out for them to be subtly central to the procedure to generate and maintain influence, while bringing service to the IC that cultivates loyalty to the products, the sales person, and the company.5 Medtech representatives and some doctors think a sales rep brings many benefits to the hospital, by amplifying productivity and offsetting deficits of procedure room staff.

Where Is This Growth Coming From?

Of the three major segments of coronary stents—BMS, DES, and bioabsorbable stents—bioabsorbable stents are expected to have the highest growth between now and 2022,6 although they represent the smallest revenue segment of the group. The worldwide bioabsorbable stent market is forecast to reach $417 million by 2022, up from $242 million in 2017 (Table 2)—a CAGR of 11.5 percent.6 Market drivers of bioresorbable stents are the growing aging population, rising percutaneous coronary intervention procedures, and increasing demand created by medical device manufacturers’ clinical trials of bioresorbable stents. There are highly regarded clinical benefits attributed to bioresorbable stents, such as a decrease in thrombosis and inflammation complications.7 One market obstacle was the high cost of bioabsorbable coronary stents when the Absorb stent from Abbott was introduced in 2016.

Table 2: Global bioabsorbable stent market revenue forecast6

Shifting the ASP Up, Up, Up

It doesn’t happen very often, but when introduced, the innovation and promise of bioabsorbable coronary stents caused an ASP shift in the upwards direction. ASP data is difficult to obtain and a 2019 article about the sales of coronary stents in India provide insights to global pricing and the power of enormous market demand in a country with a population of more than 1.4 billion people.

In February 2017, the government of India regulated the selling price of coronary stents. According to an interventional cardiologist in India, stent prices dropped by an average of 80 percent.8

Before the price was regulated, the cost to the patient of the only approved bioresorbable stent in India was 200,000 Indian Rupees (INR; approximately $2,800), compared to DES costs that ranged from INR 85,000 to 160,000 ($1,190 to $2,240). Allegations were made that hospitals and ICs obtained kickbacks for implanting stents.8

The Indian government cut and regulated stent prices significantly (Table 3). The cost for patients for a bioabsorbable stent was stabilized to INR 60,000 (approximately $840). BMS and DES were capped at INR 7,500 and 30,000, respectively ($105 and $420).8 The government reportedly used industry-supplied data while Indian physicians voiced concerns about how low profitability would drive away large stent manufacturers from supplying the newest technologies. The medical device industry pushed back, stating that supplying cardiology products at a loss would cause them to lose money, obviously to put pressure on the government. In early 2017, Abbott announced it would withdraw two stents from the Indian market after the government’s move to cap stent prices.9 The Abbott bioresorbable stent disappeared from shelves.

Table 3: Changes to stent prices in India (2017)8

The Medi-Vantage Perspective

By 2020, DES continued to dominate the overall coronary stent market and had the highest revenue market share forecasted until the end of 2024, estimated at nearly 95 percent of the total market.10 Good marketing and an intimate knowledge of pricing strategy was central to managing this enormous global market. Make price strategy a key part of your marketing and product development so the market you manage gets all the investment in development it warrants at your medical device company.

References

- bit.ly/mpo201101

- bit.ly/mpo201102

- bit.ly/mpo201103

- bit.ly/mpo201104

- bit.ly/mpo201105

- bit.ly/mpo201106

- bit.ly/mpo201107

- bit.ly/mpo201108

- bit.ly/mpo201109

- bit.ly/mpo201110

Maria Shepherd has more than 20 years of leadership experience in medical device/life-science marketing in small startups and top-tier companies. After her industry career, including her role as VP of marketing for Oridion Medical where she boosted the company valuation prior to its acquisition by Medtronic, and director of marketing for Philips Medical, she founded Medi-Vantage. Medi-Vantage provides marketing and business strategy and innovation research for the medical device industry. Shepherd has taught marketing and product development courses, speaks regularly at medtech conferences, and can be reached at mshepherd@medi-vantage. Visit her website at www.medi-vantage.com.