Maria Shepherd, President and Founder, Medi-Vantage09.01.20

Over the past 10 years, medtech manufacturers from startups to giants like Medtronic, Boston Scientific, and Abbott have grown their levels of outsourcing to contract R&D and manufacturing partners. The objective of this market shift is to gain operational efficiencies, cost savings, and access to new capabilities that provide a competitive advantage.

Medical device companies have pivoted to concentrate on their internal core competencies. Under these conditions, outsourcing makes sense in terms of cost and speed to market if medical device manufacturers select contract R&D and manufacturing partners that can expand their in-house innovation capabilities, offer scale and quality improvement, and push the fixed costs of internal R&D to the other side of the balance sheet.

The drivers of this market are continued industry consolidation (driven by hospital consolidation with more expected in the future), painful cuts in reimbursement, and the driving need to rapidly innovate. Competition is increasing from every direction such as new and emerging adjacent market players like Apple and Google, digital technologies, crossover from pharmaceutical companies in the wearables space, and unknown and possibly underestimated sources of risk such as Haven Healthcare—led by Atul Gawande, M.D., MPH, and chairman of the board, which is focused on the U.S.-based employees and families from Amazon, Berkshire Hathaway, and JPMorgan Chase.

Why This Is Important

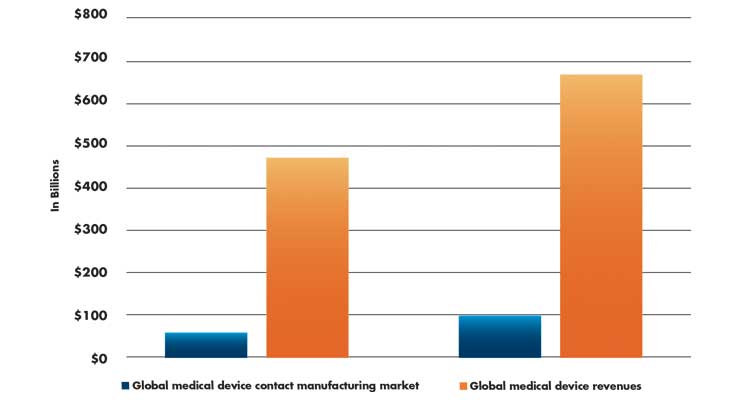

Contract medical device R&D has emerged as an industry of its own, with expertise at all the stages of the medtech lifecycle. Sheer scale is part of the reason. FDA’s CDRH reports there are approximately 175,000 categories of medical devices available in the U.S.1 Some reports put global annual medtech sales at $425 billion in 2018 and its CAGR was forecasted (pre-COVID) to grow at approximately 5.4 percent for the near future, placing the market in 2027 at approximately $680 billion.2 Few medical device developers have the basic but broad technical expertise and resources to develop products in-house. There is a high cost to acquire that required infrastructure and expertise.

Medtech companies have limited finances (and all have limited budgets, especially now, in the COVID era) to maintain and manage complicated R&D programs. In addition, regulations are changing. Human factors usability testing has been mandatory since 2016 and the EU’s revised MDR will require medical devices to undergo exacting quality programs, which further escalates the need for expertise and dedicated resources. COVID-19 has delayed the enforcement of the EU’s MDR until May 2021, which will be here before we know it, so this is a “can” medical device companies cannot continue to kick down the road. Medtech manufacturers also expect outsourcing to yield cost savings and faster time to market. These are all drivers of the outsourcing of R&D, manufacturing, clinical research, and regulatory affairs.

This growth will be substantial. For example, the global medtech contract manufacturing market is expected to grow to almost $100 billion by 2027 (Table 1), a CAGR of approximately 7 percent.3

Table 1: Growth in global medical device and contract manufacturing markets between 2020 and 20272,3

Specialization in the Medtech Outsourced Services Market

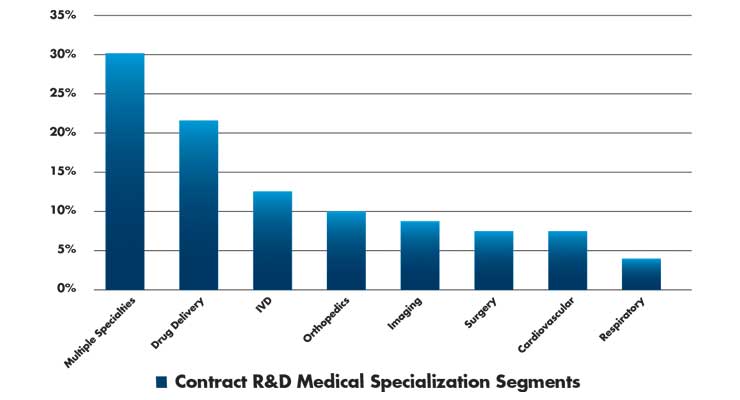

According to a recent report by MassMEDIC, contract R&D services are specializing in recognition of the need for specific services by medical specialty.4 The areas of highest growth are drug delivery, IVD consumables, and robotic-assisted surgical systems (Table 2). These are the areas where market demand is proven and has shown sustainability. The two largest markets—cardiovascular and orthopedic devices—may require high performance materials, manufacturing, or end-use market demand, such as digital health or drug delivery.

Table 2: 2025 expected market segments for contract R&D specialized focus4

Critical Success Factors

While the medical device contract R&D and manufacturing market is highly fragmented, there are competitive trends all must recognize to be successful. Expect and plan for the following:

Medtech Patents in U.S. Regional Clusters

The U.S. is the single largest medical device market in the world with a market size of approximately $156 billion in 2017.5 There are greater than 6,500 medical device companies in the U.S., mostly small- and medium-sized businesses. Greater than 80 percent of medtech companies have fewer than 50 employees. Most are pre-commercial, with little or no sales revenue.

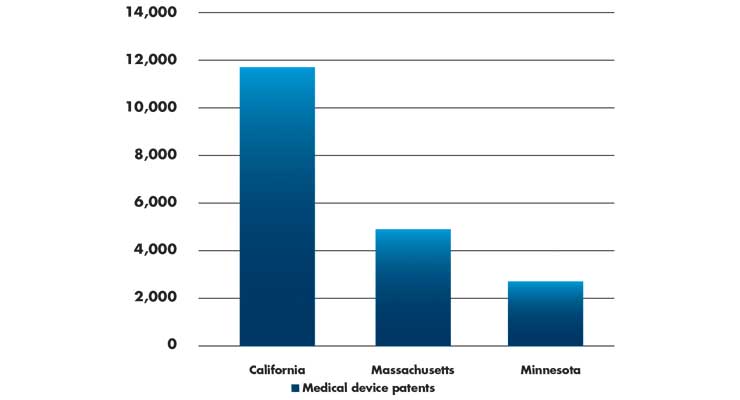

Access to medical device clusters is critical to the success of medical device contract R&D and manufacturing companies. California, Massachusetts, and Minnesota are three of the leading states for medical device patent registrations in the U.S. (Table 3). Medical device patents registered in the U.S. in 2019 totaled 51,803.6

Table 3: Medical device patents by state6

The Medi-Vantage Perspective

U.S. medtech companies are still dominant in their global position as innovators and developers of high technology products. Company investment in medtech R&D more than doubled during the 1990s. However, R&D investment declined to 4.7 percent between 2013 and 2017 from an average of 15.5 percent between 2000 and 2007. If the medtech trend of under-investing in R&D continues, what happens to the dominant position of the U.S. in medical device innovation?

In these clusters, medical device contract R&D and manufacturing companies have large groups of potential early-stage customers who have received investment and whose technology can, over time, develop into successful businesses. The trick is in identifying the winners and losers.

References

Maria Shepherd has more than 20 years of leadership experience in medical device/life-science marketing in small startups and top-tier companies. After her industry career, including her role as vice president of marketing for Oridion Medical where she boosted the company valuation prior to its acquisition by Medtronic, director of marketing for Philips Medical, and senior management roles at Boston Scientific Corp., she founded Medi-Vantage. Medi-Vantage provides marketing and business strategy and innovation research for the medical device industry. The firm quantitatively and qualitatively sizes and segments opportunities, evaluates new technologies, provides marketing services, and assesses prospective acquisitions. Shepherd has taught marketing and product development courses, speaks regularly at medtech conferences, and can be reached at mshepherd@medi-vantage. Visit her website at www.medi-vantage.com.

Medical device companies have pivoted to concentrate on their internal core competencies. Under these conditions, outsourcing makes sense in terms of cost and speed to market if medical device manufacturers select contract R&D and manufacturing partners that can expand their in-house innovation capabilities, offer scale and quality improvement, and push the fixed costs of internal R&D to the other side of the balance sheet.

The drivers of this market are continued industry consolidation (driven by hospital consolidation with more expected in the future), painful cuts in reimbursement, and the driving need to rapidly innovate. Competition is increasing from every direction such as new and emerging adjacent market players like Apple and Google, digital technologies, crossover from pharmaceutical companies in the wearables space, and unknown and possibly underestimated sources of risk such as Haven Healthcare—led by Atul Gawande, M.D., MPH, and chairman of the board, which is focused on the U.S.-based employees and families from Amazon, Berkshire Hathaway, and JPMorgan Chase.

Why This Is Important

Contract medical device R&D has emerged as an industry of its own, with expertise at all the stages of the medtech lifecycle. Sheer scale is part of the reason. FDA’s CDRH reports there are approximately 175,000 categories of medical devices available in the U.S.1 Some reports put global annual medtech sales at $425 billion in 2018 and its CAGR was forecasted (pre-COVID) to grow at approximately 5.4 percent for the near future, placing the market in 2027 at approximately $680 billion.2 Few medical device developers have the basic but broad technical expertise and resources to develop products in-house. There is a high cost to acquire that required infrastructure and expertise.

Medtech companies have limited finances (and all have limited budgets, especially now, in the COVID era) to maintain and manage complicated R&D programs. In addition, regulations are changing. Human factors usability testing has been mandatory since 2016 and the EU’s revised MDR will require medical devices to undergo exacting quality programs, which further escalates the need for expertise and dedicated resources. COVID-19 has delayed the enforcement of the EU’s MDR until May 2021, which will be here before we know it, so this is a “can” medical device companies cannot continue to kick down the road. Medtech manufacturers also expect outsourcing to yield cost savings and faster time to market. These are all drivers of the outsourcing of R&D, manufacturing, clinical research, and regulatory affairs.

This growth will be substantial. For example, the global medtech contract manufacturing market is expected to grow to almost $100 billion by 2027 (Table 1), a CAGR of approximately 7 percent.3

Table 1: Growth in global medical device and contract manufacturing markets between 2020 and 20272,3

Specialization in the Medtech Outsourced Services Market

According to a recent report by MassMEDIC, contract R&D services are specializing in recognition of the need for specific services by medical specialty.4 The areas of highest growth are drug delivery, IVD consumables, and robotic-assisted surgical systems (Table 2). These are the areas where market demand is proven and has shown sustainability. The two largest markets—cardiovascular and orthopedic devices—may require high performance materials, manufacturing, or end-use market demand, such as digital health or drug delivery.

Table 2: 2025 expected market segments for contract R&D specialized focus4

Critical Success Factors

While the medical device contract R&D and manufacturing market is highly fragmented, there are competitive trends all must recognize to be successful. Expect and plan for the following:

- Technical differentiation is a critical success factor that allows medical device contract R&D and manufacturing providers to maintain prices or charge a slight price premium.

- Vertically integrated competitors recognize and are aligning their core strengths and footprint with the medical specialty they serve.

- More consolidation in the medical device contract R&D and manufacturing industry is coming, following the trends set by hospitals and medtech manufacturers.

- Target early in product development, while emphasizing strengths upstream, with a high focus on quality to be able to serve medtech throughout the lifecycle of the device.

- Establish long-term partnerships that can serve as a highly credible proof source to expand business at large medical device manufacturers.

- Maintain margins through outsourcing less-competitive R&D activities such as injection molding.

Medtech Patents in U.S. Regional Clusters

The U.S. is the single largest medical device market in the world with a market size of approximately $156 billion in 2017.5 There are greater than 6,500 medical device companies in the U.S., mostly small- and medium-sized businesses. Greater than 80 percent of medtech companies have fewer than 50 employees. Most are pre-commercial, with little or no sales revenue.

Access to medical device clusters is critical to the success of medical device contract R&D and manufacturing companies. California, Massachusetts, and Minnesota are three of the leading states for medical device patent registrations in the U.S. (Table 3). Medical device patents registered in the U.S. in 2019 totaled 51,803.6

Table 3: Medical device patents by state6

The Medi-Vantage Perspective

U.S. medtech companies are still dominant in their global position as innovators and developers of high technology products. Company investment in medtech R&D more than doubled during the 1990s. However, R&D investment declined to 4.7 percent between 2013 and 2017 from an average of 15.5 percent between 2000 and 2007. If the medtech trend of under-investing in R&D continues, what happens to the dominant position of the U.S. in medical device innovation?

In these clusters, medical device contract R&D and manufacturing companies have large groups of potential early-stage customers who have received investment and whose technology can, over time, develop into successful businesses. The trick is in identifying the winners and losers.

References

Maria Shepherd has more than 20 years of leadership experience in medical device/life-science marketing in small startups and top-tier companies. After her industry career, including her role as vice president of marketing for Oridion Medical where she boosted the company valuation prior to its acquisition by Medtronic, director of marketing for Philips Medical, and senior management roles at Boston Scientific Corp., she founded Medi-Vantage. Medi-Vantage provides marketing and business strategy and innovation research for the medical device industry. The firm quantitatively and qualitatively sizes and segments opportunities, evaluates new technologies, provides marketing services, and assesses prospective acquisitions. Shepherd has taught marketing and product development courses, speaks regularly at medtech conferences, and can be reached at mshepherd@medi-vantage. Visit her website at www.medi-vantage.com.