Bill Ellerkamp, Contributing Writer05.03.18

The first quarter of 2018 has been particularly busy with M&A activity in the medical device outsourced manufacturing market. The industry has seen the largest number of closed acquisitions in any first quarter over the last three years. It’s also seen a steady increase from six in 2016 to 10 in 2017 and 11 in 2018. The majority of the Q1 activity was related to private sellers of relatively small businesses to strategic buyers. Following are highlights of a few of those deals and a summary of Q1 deal activity.

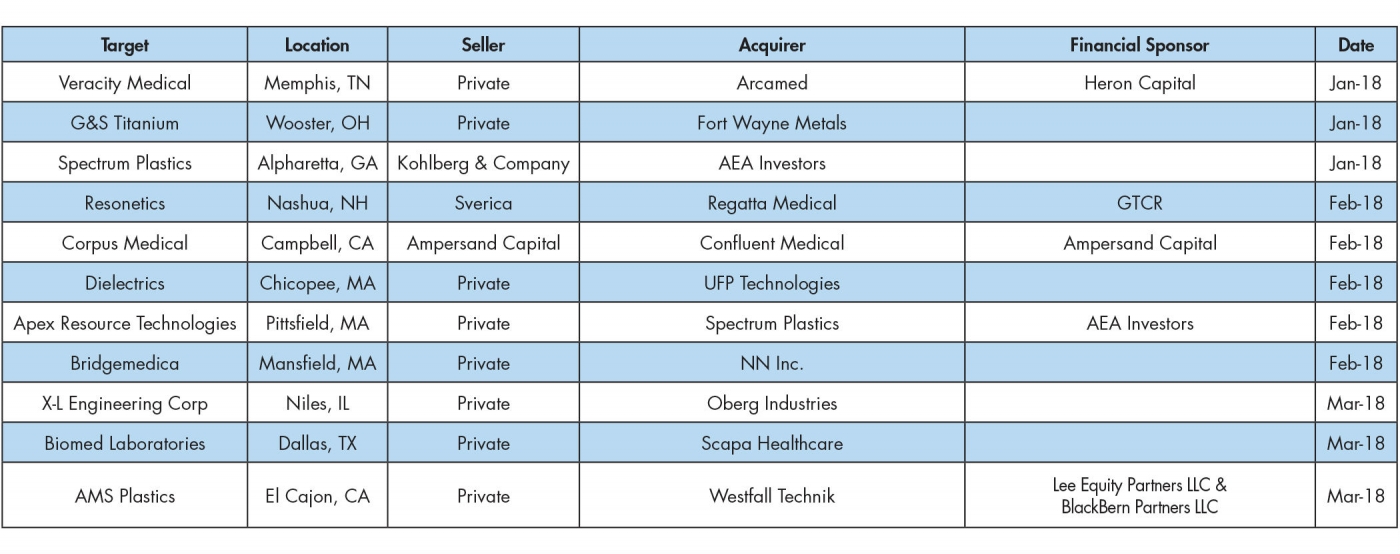

The biggest deal of Q1 was the acquisition of Spectrum Plastics by AEA Investors in January. This came close on the heels of Kohlberg & Company’s acquisition of Pexco and merger with their PPC Industries platform business in February 2017 to form Spectrum Plastics. AEA didn’t waste any time following up on that deal with the add-on acquisition of Apex Resource Technologies in February. Spectrum Plastics is becoming a formidable platform, with a broad plastics portfolio, including extrusion, molding, and contract manufacturing of thermoplastics, silicone, and bioresorbable materials. Meanwhile, Kohlberg & Company didn’t waste any time either in getting back into the space with the April announcement of its acquisition of Cadence.

It may have been a bit of a surprise to see Resonetics announce a new investor in Q1 after just over three years with Sverica Capital Management, but both Sverica and CEO Tom Burns are staying involved. Also, it looks like new investors, Regatta Medical/GTCR, will help Resonetics maintain, or accelerate, the impressive pace of both internal expansion and acquisitions. During the Sverica hold period, Resonetics expanded from one to six facilities, closing several acquisitions (including Aduro Laser in Q3 2017), expanding services, and bringing its broad range of laser services closer to customers.

NN Inc. has been quietly transforming itself from a diversified industrial engineered components business to a more medical device engineered products orientation. Since 2015, they have completed a number of acquisitions in precision machining and contract manufacturing, largely addressing the surgical instrumentation and orthopedics market segments. In February, they added Bridgemedica—a design-develop-manufacture services provider that will strengthen the “front end” of the NN medical customer collaboration model—which closely followed the acquisition of DRT Medical in October 2017. And, more recently, in April, NN announced the acquisition of Paragon Medical —a manufacturer that focuses on the orthopedic case and tray, implant, and instrument markets. NN is rapidly approaching $500 million in revenue in its Life Sciences division and is definitely a company to keep an eye on in the future.

It was not a surprise to see Corpus Medical merged into Confluent Medical in February. Both companies are platform businesses, addressing overlapping markets and customers, and sponsored by Ampersand Capital. Ampersand had engineered a similar merger of another platform business, ETE Medical, into Confluent in the second half of 2016. These were logical moves that only serve to strengthen Confluent Medical and its strong position in vascular intervention markets.

A new platform business to watch out for is Westfall Technik, led by Brian Jones—the former CEO of Nypro—and backed by private equity groups Lee Equity Partners and Blackbern Partners. Westfall Technik is a plastics molding and manufacturing services network that completed a third acquisition in Q1, and in April, announced the acquisition of AMA Plastics. While the business serves diverse markets, it is rapidly building a position in medtech outsourced manufacturing.

2017 in Review

Actual deals closed in 2017 decreased somewhat from 2016 and may not reflect the level of interest and effort that went into M&A activity during the year. Business development strategies, whether they be corporate or private equity buyers, are becoming more sophisticated and nuanced while M&A activities are more focused and targeted.

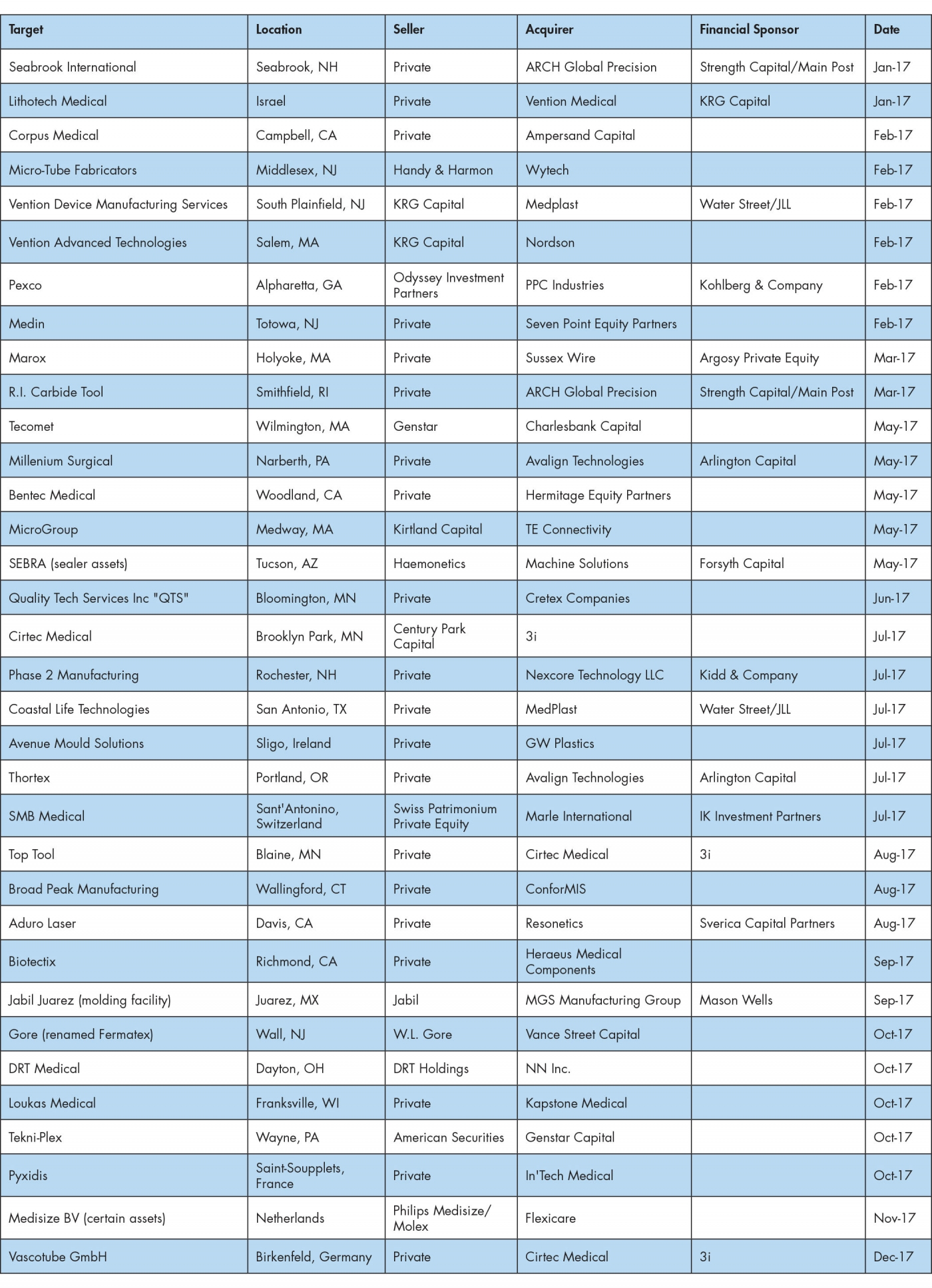

The biggest deal of 2017—and also the one that created significant buzz in the industry—was the sale of Vention into two pieces to Nordson and Medplast respectively. Nordson acquired the Advanced Technologies division and Medplast acquired the Device Manufacturing Services division. These two businesses added significant critical mass, competencies, and customer relationships to both buyers, and should help propel both Nordson and Medplast to stronger, more defensible positions in their respective segments of the industry. Medplast quickly followed up the Vention acquisition with another deal for Coastal Life Technologies in July 2017.

The orthopedic market gained substantial attention during 2017, led by Tecomet returning to Charlesbank Capital after a sojourn with Genstar. Other notable deals were Avalign’s investments in Millenium Surgical and Thortex. The addition of Thortex’s porous implant coating capability for Avalign, in particular, will strengthen the firm’s competitiveness vis-a-vis Tecomet and Orchid. ARCH Global Precision continued its acquisition run, adding Seabrook International and RI Carbide Tool during 2017. Two case and tray manufacturers also traded during the year—Medin and Pyxidis.

Genstar didn’t waste any time in plowing back into the medtech outsourced manufacturing space with its acquisition of Tekni-Plex late in 2017. Further, the company just announced in April the first Tekni-Plex add-on acquisition of Dunn Industries—a manufacturer of specialty extrusion tubing for medical device applications.

An exciting new platform business is being rapidly built by 3i Group, starting with the acquisition of Cirtec Medical in July 2017, followed quickly by the addition of Top Tool in August and Vascotube in December. The group is very much focused on design, development, and manufacturing of active implants and minimally invasive devices for some of the most sophisticated and high-growth medtech segments, including neurostimulation, vascular intervention and implants, and structural heart.

A strategic buyer that has consistently been making a significant transformation in its business model toward medical is Cretex—a privately owned company that began life as an aggregates supplier to the asphalt and concrete industry supporting the building of road systems in the first half of the 20th century. In June, Cretex acquired Quality Tech Services—a medical device packaging and outsourcing services provider—in a move that expanded its medtech services offering, which already included JunoPacific, rms, Spectralytics, and several other outsourced manufacturing services providers.

A phenomenon the industry hasn’t seen much of in medtech contract manufacturing has been carve outs, where buyers have acquired operating units or facilities of other entities that are no longer a good strategic fit, or are excess to capacity requirements. In 2017, there were four notable carve-outs, starting with Machine Solutions’ acquisition in May of Haemonetics’ SEBRA line of benchtop and hand sealer equipment for blood and plasma centers worldwide. It was a relatively small deal, but certainly seemed to be a better fit with Machine Solutions than Haemonetics. A much more significant carve-out was MGS Manufacturing Group’s acquisition in September of a 125,000-square-foot Jabil injection molding facility in Juarez, Mexico. This was formerly a Nypro facility and added significant capacity, at a lower cost basis, for MGS—a Mason Wells platform business. Vance Street Capital continued its investment in medtech with the October acquisition of a W.L. Gore facility in New Jersey, which was the former Adam Spence Corporation business. This business is a manufacturer of high-pressure braided tubing, complex medical extrusions, and advanced catheters, which Vance Street has rebranded as Fermatex Vascular Technologies. Lastly, in November, Phillips-Medisize divested itself of certain European assets in the Netherlands, Germany, and Italy associated with the supply and distribution of respiratory and anesthesia products. These assets were sold to Flexicare out of the United Kingdom, and really completed the transition of Phillips-Medisize to a pure outsourcing business model following its acquisition by Molex in 2016.

Outlook for 2018

In discussions with industry participants over the last two quarters, optimism remains high for the state of the industry. The recent tax package was well received, particularly the suspension of the 2.3 percent medical device excise tax for an additional two years—which was birthed from the Affordable Care Act—as well as the lower business tax rates and extension of bonus depreciation. More recent events, specifically the prospect of a repeal of NAFTA and new tariffs, may pose some threats to an industry becoming more dependent on manufacturing in Mexico, the Caribbean basin, and China.

With respect to deal activity, the industry may see some shift toward market segments that are generally trading at lower multiples, notably orthopedics and surgical instrumentation. In addition, there may be a continuing trend in the short term favoring smaller deals as some of the recent consolidators work through integration issues and look to fill gaps in their portfolios. Having said that, the appetite for deals in this space from a wide variety of buyers continues to be robust, in spite of historically high valuations. This reflects a number of positive trends, including favorable demographics, healthcare spending trends, demand for innovation, and attractive/stable revenue and profitability. According to several recent market analyses, the market for contract manufacturing and outsourced services in the global medical device industry is projected to grow by double digits for the foreseeable future.

This is a highly attractive industry to consolidators, both strategic and financial, for several reasons.

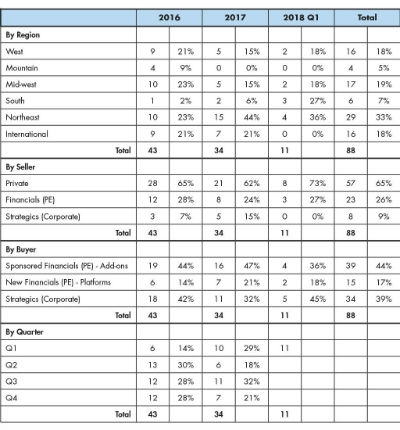

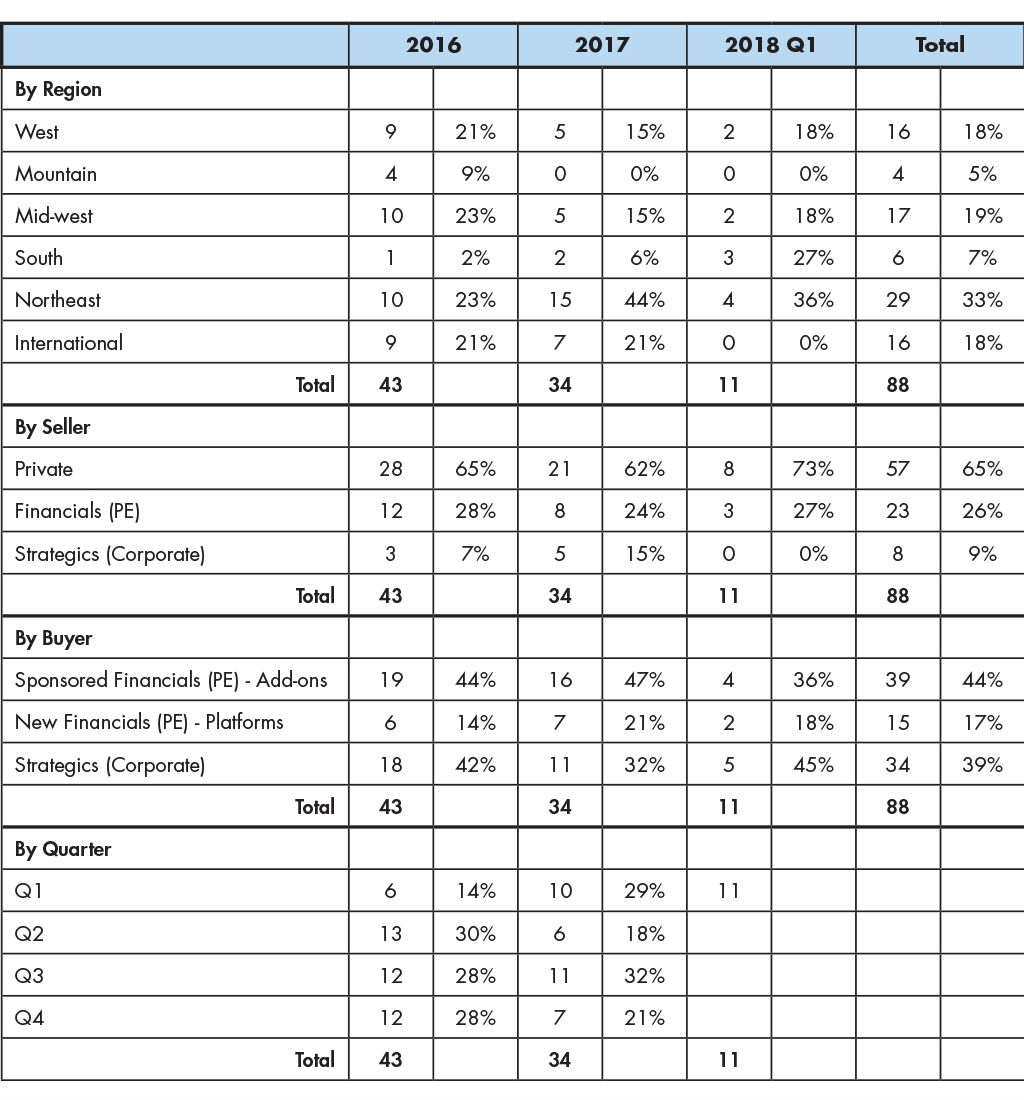

Summary Medtech Outsourced Manufacturing Deals 2016-2018. (Click the table to view a larger version.)

Industry dynamics continue to shift toward favoring larger outsourced manufacturing partners, and scale requirements are still quite low by many industry standards. We still see only a handful of contract manufacturers that have passed the $1 billion mark, and it is still possible to establish industry-leading positions in select sub-segments of the market at revenue levels starting not far above $100 million.

It is still quite fragmented, with a large number of small, founder-owner players in the $5 million to $20 million range. Lower middle market private equity has been quite active in doing the heavy lifting associated with integrating smaller consolidations and are presenting operationally and strategically positioned $50 million-plus businesses to strategic buyers, as well as larger financial buyers with existing portfolio businesses, for acquisition.

There are substantial engineered component plays to be done, which are particularly attractive to industrial buyers looking for diversification plays and entry points into this attractive industry, who are more comfortable with the margin and risk profiles of these businesses.

Who’s Buying

Financial buyers, particularly sponsors who are pursuing add-on acquisitions for platform businesses in their current portfolios, are very active. Quite a few PE firms have developed substantial experience in medtech outsourced manufacturing across multiple platforms in a variety of segments, including Genstar Capital, Kohlberg & Company, Water Street Healthcare Partners, KRG Capital, Ampersand, 3i, Mason Wells, Altaris, Inverness Graham Investments, Linden Capital Partners, Vance Street Capital, and others. These firms all have had successes in this business, have access to plenty of capital, and are enthusiastic about putting more of their money to work in this attractive market.

Strategic (or corporate) buyers continue to become increasingly active in acquisition activity. There was speculation some corporates were staying on the sidelines due to the high valuations, but it seems they may be learning how to get more creative with their strategies and more aggressive with their pricing. This buying group represents approximately 40 percent of all acquisitions since 2016, and an even higher percentage in Q1 2018. We haven’t seen much activity from international (mainly European) corporate buyers in 2018 (or 2017, for that matter), although there was certainly plenty of activity from that group in 2016. This may reflect a cautious approach to the policies and potential volatility of the new administration.

Who’s Selling?

A very significant two-thirds of all sellers since the beginning of 2016 have been private, mainly founder-owners. This trend was particularly pronounced in Q1 2018, with almost three-quarters of all sellers being private. There is a very large inventory of companies in the medtech outsourced manufacturing industry with founder-owners approaching retirement who have no clear succession plan. This will continue to fuel deal flow in this industry for the foreseeable future.

Adding to that will be the accelerating platform builds of private equity groups, particularly lower middle market and middle market PEs, which have a typical ±five-year-hold period. A significant number of current PE-owned platforms will be approaching their maturity over the next 12 to 18 months and the industry can expect to see some very attractive platforms coming to market in that period and beyond.

Bill Ellerkamp is a medical device industry executive and strategic advisor. He has more than 35-years of operating experience, primarily in medtech contract manufacturing. He currently serves on several boards and, through his consulting group, Acceleration Medtech, provides advisory services to private equity firms, corporations, and independent business owners on strategy, market assessment, business development, operational planning, buy- and sell-side planning, and due diligence. He can be reached at bill.ellerkamp@gmail.com.

The biggest deal of Q1 was the acquisition of Spectrum Plastics by AEA Investors in January. This came close on the heels of Kohlberg & Company’s acquisition of Pexco and merger with their PPC Industries platform business in February 2017 to form Spectrum Plastics. AEA didn’t waste any time following up on that deal with the add-on acquisition of Apex Resource Technologies in February. Spectrum Plastics is becoming a formidable platform, with a broad plastics portfolio, including extrusion, molding, and contract manufacturing of thermoplastics, silicone, and bioresorbable materials. Meanwhile, Kohlberg & Company didn’t waste any time either in getting back into the space with the April announcement of its acquisition of Cadence.

It may have been a bit of a surprise to see Resonetics announce a new investor in Q1 after just over three years with Sverica Capital Management, but both Sverica and CEO Tom Burns are staying involved. Also, it looks like new investors, Regatta Medical/GTCR, will help Resonetics maintain, or accelerate, the impressive pace of both internal expansion and acquisitions. During the Sverica hold period, Resonetics expanded from one to six facilities, closing several acquisitions (including Aduro Laser in Q3 2017), expanding services, and bringing its broad range of laser services closer to customers.

NN Inc. has been quietly transforming itself from a diversified industrial engineered components business to a more medical device engineered products orientation. Since 2015, they have completed a number of acquisitions in precision machining and contract manufacturing, largely addressing the surgical instrumentation and orthopedics market segments. In February, they added Bridgemedica—a design-develop-manufacture services provider that will strengthen the “front end” of the NN medical customer collaboration model—which closely followed the acquisition of DRT Medical in October 2017. And, more recently, in April, NN announced the acquisition of Paragon Medical —a manufacturer that focuses on the orthopedic case and tray, implant, and instrument markets. NN is rapidly approaching $500 million in revenue in its Life Sciences division and is definitely a company to keep an eye on in the future.

It was not a surprise to see Corpus Medical merged into Confluent Medical in February. Both companies are platform businesses, addressing overlapping markets and customers, and sponsored by Ampersand Capital. Ampersand had engineered a similar merger of another platform business, ETE Medical, into Confluent in the second half of 2016. These were logical moves that only serve to strengthen Confluent Medical and its strong position in vascular intervention markets.

A new platform business to watch out for is Westfall Technik, led by Brian Jones—the former CEO of Nypro—and backed by private equity groups Lee Equity Partners and Blackbern Partners. Westfall Technik is a plastics molding and manufacturing services network that completed a third acquisition in Q1, and in April, announced the acquisition of AMA Plastics. While the business serves diverse markets, it is rapidly building a position in medtech outsourced manufacturing.

2017 in Review

Actual deals closed in 2017 decreased somewhat from 2016 and may not reflect the level of interest and effort that went into M&A activity during the year. Business development strategies, whether they be corporate or private equity buyers, are becoming more sophisticated and nuanced while M&A activities are more focused and targeted.

The biggest deal of 2017—and also the one that created significant buzz in the industry—was the sale of Vention into two pieces to Nordson and Medplast respectively. Nordson acquired the Advanced Technologies division and Medplast acquired the Device Manufacturing Services division. These two businesses added significant critical mass, competencies, and customer relationships to both buyers, and should help propel both Nordson and Medplast to stronger, more defensible positions in their respective segments of the industry. Medplast quickly followed up the Vention acquisition with another deal for Coastal Life Technologies in July 2017.

The orthopedic market gained substantial attention during 2017, led by Tecomet returning to Charlesbank Capital after a sojourn with Genstar. Other notable deals were Avalign’s investments in Millenium Surgical and Thortex. The addition of Thortex’s porous implant coating capability for Avalign, in particular, will strengthen the firm’s competitiveness vis-a-vis Tecomet and Orchid. ARCH Global Precision continued its acquisition run, adding Seabrook International and RI Carbide Tool during 2017. Two case and tray manufacturers also traded during the year—Medin and Pyxidis.

Genstar didn’t waste any time in plowing back into the medtech outsourced manufacturing space with its acquisition of Tekni-Plex late in 2017. Further, the company just announced in April the first Tekni-Plex add-on acquisition of Dunn Industries—a manufacturer of specialty extrusion tubing for medical device applications.

An exciting new platform business is being rapidly built by 3i Group, starting with the acquisition of Cirtec Medical in July 2017, followed quickly by the addition of Top Tool in August and Vascotube in December. The group is very much focused on design, development, and manufacturing of active implants and minimally invasive devices for some of the most sophisticated and high-growth medtech segments, including neurostimulation, vascular intervention and implants, and structural heart.

A strategic buyer that has consistently been making a significant transformation in its business model toward medical is Cretex—a privately owned company that began life as an aggregates supplier to the asphalt and concrete industry supporting the building of road systems in the first half of the 20th century. In June, Cretex acquired Quality Tech Services—a medical device packaging and outsourcing services provider—in a move that expanded its medtech services offering, which already included JunoPacific, rms, Spectralytics, and several other outsourced manufacturing services providers.

A phenomenon the industry hasn’t seen much of in medtech contract manufacturing has been carve outs, where buyers have acquired operating units or facilities of other entities that are no longer a good strategic fit, or are excess to capacity requirements. In 2017, there were four notable carve-outs, starting with Machine Solutions’ acquisition in May of Haemonetics’ SEBRA line of benchtop and hand sealer equipment for blood and plasma centers worldwide. It was a relatively small deal, but certainly seemed to be a better fit with Machine Solutions than Haemonetics. A much more significant carve-out was MGS Manufacturing Group’s acquisition in September of a 125,000-square-foot Jabil injection molding facility in Juarez, Mexico. This was formerly a Nypro facility and added significant capacity, at a lower cost basis, for MGS—a Mason Wells platform business. Vance Street Capital continued its investment in medtech with the October acquisition of a W.L. Gore facility in New Jersey, which was the former Adam Spence Corporation business. This business is a manufacturer of high-pressure braided tubing, complex medical extrusions, and advanced catheters, which Vance Street has rebranded as Fermatex Vascular Technologies. Lastly, in November, Phillips-Medisize divested itself of certain European assets in the Netherlands, Germany, and Italy associated with the supply and distribution of respiratory and anesthesia products. These assets were sold to Flexicare out of the United Kingdom, and really completed the transition of Phillips-Medisize to a pure outsourcing business model following its acquisition by Molex in 2016.

Outlook for 2018

In discussions with industry participants over the last two quarters, optimism remains high for the state of the industry. The recent tax package was well received, particularly the suspension of the 2.3 percent medical device excise tax for an additional two years—which was birthed from the Affordable Care Act—as well as the lower business tax rates and extension of bonus depreciation. More recent events, specifically the prospect of a repeal of NAFTA and new tariffs, may pose some threats to an industry becoming more dependent on manufacturing in Mexico, the Caribbean basin, and China.

With respect to deal activity, the industry may see some shift toward market segments that are generally trading at lower multiples, notably orthopedics and surgical instrumentation. In addition, there may be a continuing trend in the short term favoring smaller deals as some of the recent consolidators work through integration issues and look to fill gaps in their portfolios. Having said that, the appetite for deals in this space from a wide variety of buyers continues to be robust, in spite of historically high valuations. This reflects a number of positive trends, including favorable demographics, healthcare spending trends, demand for innovation, and attractive/stable revenue and profitability. According to several recent market analyses, the market for contract manufacturing and outsourced services in the global medical device industry is projected to grow by double digits for the foreseeable future.

This is a highly attractive industry to consolidators, both strategic and financial, for several reasons.

Summary Medtech Outsourced Manufacturing Deals 2016-2018. (Click the table to view a larger version.)

It is still quite fragmented, with a large number of small, founder-owner players in the $5 million to $20 million range. Lower middle market private equity has been quite active in doing the heavy lifting associated with integrating smaller consolidations and are presenting operationally and strategically positioned $50 million-plus businesses to strategic buyers, as well as larger financial buyers with existing portfolio businesses, for acquisition.

There are substantial engineered component plays to be done, which are particularly attractive to industrial buyers looking for diversification plays and entry points into this attractive industry, who are more comfortable with the margin and risk profiles of these businesses.

Who’s Buying

Financial buyers, particularly sponsors who are pursuing add-on acquisitions for platform businesses in their current portfolios, are very active. Quite a few PE firms have developed substantial experience in medtech outsourced manufacturing across multiple platforms in a variety of segments, including Genstar Capital, Kohlberg & Company, Water Street Healthcare Partners, KRG Capital, Ampersand, 3i, Mason Wells, Altaris, Inverness Graham Investments, Linden Capital Partners, Vance Street Capital, and others. These firms all have had successes in this business, have access to plenty of capital, and are enthusiastic about putting more of their money to work in this attractive market.

Strategic (or corporate) buyers continue to become increasingly active in acquisition activity. There was speculation some corporates were staying on the sidelines due to the high valuations, but it seems they may be learning how to get more creative with their strategies and more aggressive with their pricing. This buying group represents approximately 40 percent of all acquisitions since 2016, and an even higher percentage in Q1 2018. We haven’t seen much activity from international (mainly European) corporate buyers in 2018 (or 2017, for that matter), although there was certainly plenty of activity from that group in 2016. This may reflect a cautious approach to the policies and potential volatility of the new administration.

Who’s Selling?

A very significant two-thirds of all sellers since the beginning of 2016 have been private, mainly founder-owners. This trend was particularly pronounced in Q1 2018, with almost three-quarters of all sellers being private. There is a very large inventory of companies in the medtech outsourced manufacturing industry with founder-owners approaching retirement who have no clear succession plan. This will continue to fuel deal flow in this industry for the foreseeable future.

Adding to that will be the accelerating platform builds of private equity groups, particularly lower middle market and middle market PEs, which have a typical ±five-year-hold period. A significant number of current PE-owned platforms will be approaching their maturity over the next 12 to 18 months and the industry can expect to see some very attractive platforms coming to market in that period and beyond.

Bill Ellerkamp is a medical device industry executive and strategic advisor. He has more than 35-years of operating experience, primarily in medtech contract manufacturing. He currently serves on several boards and, through his consulting group, Acceleration Medtech, provides advisory services to private equity firms, corporations, and independent business owners on strategy, market assessment, business development, operational planning, buy- and sell-side planning, and due diligence. He can be reached at bill.ellerkamp@gmail.com.