Mihir Torsekar, International Trade Analyst, U.S. International Trade Commission01.29.18

Renegotiations for the North American Free Trade Agreement (NAFTA) kicked off in August 2017, making this an opportune time to discuss the impact the trade agreement has made on the region’s medical goods supply chain. The trade agreement, which links the markets of the U.S., Mexico, and Canada, has been in place since 1994 and has principally facilitated the expansion of regional medical goods trade through the application of duty-free treatment on these goods.

Since NAFTA’s inception, total trade in medical products between the U.S. and its NAFTA partners has expanded by nearly 760 percent, reaching $16.5 billion in 2016—eclipsing the growth rate observed between the U.S. and other key markets such as the European Union or East Asia, as well as the rest of the world over the 22-year period. The bulk of regional trade consists of surgical instruments (40 percent); disposable goods, such as hospital supplies (24 percent); and therapeutic devices, such as orthopedic devices, hearing aids, and pacemakers (19 percent).

NAFTA has also facilitated increased trade in industries related to the medical goods manufacturing industry. For example, the U.S. plastics industry claimed to have tallied $29.7 billion in exports to Canada and Mexico during 2016—nearly half of all U.S. plastics exports for the year. Plastics are commonly used for manufacturing devices ranging from surgical instruments to components used in diagnostic technologies.

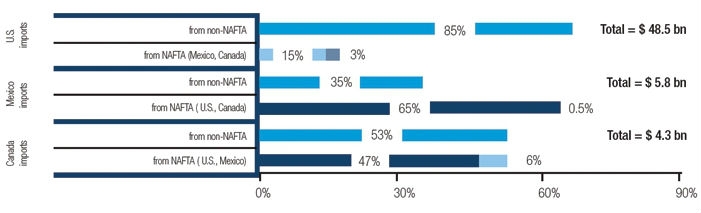

Figure 1: In 2016, the United States was by far the single largest supplier of medical devices to Canada and Mexico, while Mexico was the largest source of medical devices for the United States (% share). [Source: Compiled by author from IHS Markit, Global Trade Atlas (accessed September 2017).]

Each country in the pact has played a distinct role in this trade story: Mexico has served as an attractive destination for U.S. medical product manufacturers to locate low-cost, less-sophisticated elements of its supply chain; the U.S. has been the region’s predominant supplier of high-end equipment, such as diagnostic technologies, as well as the region’s largest consuming market for medical goods (Figure 1); and Canada, while not as sizeable a market as the U.S., has played a critical role in importing much of the United States’ high-end technologies, such as orthopedic devices, intravenous diagnostic equipment, and various diagnostic technologies. Following is a summary of the four key takeaways from NAFTA.

1. The U.S. trade deficit with its NAFTA partners has increased in recent years.

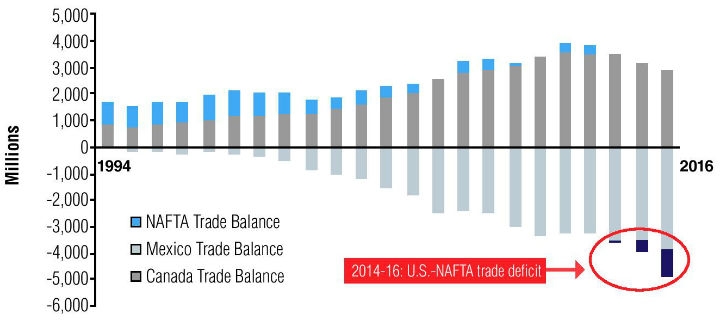

A stated objective of Robert Lighthizer, the U.S. Trade Representative, has been to reduce the U.S. trade deficit with NAFTA partners. Notably, medical goods manufacturing is one of the few industries in the U.S. that regularly maintains a trade surplus with its global trading partners. In the early years after NAFTA’s inception, the U.S. maintained this trend with its regional trading partners, due primarily to robust Canadian imports of surgical equipment, implantable devices, and intravenous diagnostic equipment from the U.S. However, this trend has reversed in recent years; every year since 2014, the U.S. has witnessed a widening trade deficit for medical goods, which reached $1 billion in 2016 (Figure 2). This development has reflected slightly reduced imports of medical goods into Canada’s maturing medical device market. At the same time, the U.S. bilateral trade deficit with Mexico has remained consistent, driven largely by U.S. imports of surgical equipment from Mexico.

Figure 2: The U.S.-NAFTA trade deficit for medical devices has been increasing since 2014 (billion $). [Source: Compiled by author from IHS Markit, Global Trade Atlas (accessed September 2017).]

2. U.S.-Mexico medical products trade is driven by parts and low-value-added goods.

More than two-thirds of North American medical goods trade is attributable to bilateral trade between Mexico and the U.S. As of 2016, Mexico has emerged as the United States’ largest trading partner of these products. Total trade between these countries principally consists of parts—such as plastic components for intravenous drug delivery catheters; steel used for orthopedic implants; and electronic components used for devices ranging from pacemakers to diagnostic equipment—that are used for manufacturing finished equipment in the U.S.; surgical equipment; and basic hospital supplies, such as first aid kits and surgical gloves.

Of particular note is the United States’ heavy reliance on Mexico to supply parts that are used in the eventual production of finished goods. For example, over the past decade, Mexico has accounted for more than half of the United States’ imports of parts for cardiac pacemakers. Overall, Mexico has been the largest source of U.S. medical goods imports since 2009.

Since NAFTA’s passage, U.S. firms have relocated much of their labor-intensive manufacturing activities to Mexico in an attempt to take advantage of the country’s relatively low labor costs; nearly 90 percent of U.S. investments into Mexico’s medical device sector were directed toward manufacturing during 2003–16. Further, wages for medical device technicians in Tijuana—Mexico’s largest medical device producing city—are roughly 44 percent less than similar jobs in the U.S. according to the New York Times. In contrast, most of the high-value added activities, such as research and development, are largely conducted in the U.S.

3. Medical device clusters in Mexico and the U.S. have driven total regional trade.

Mexico’s proximity to the U.S.—the world’s largest medical device market—coupled with NAFTA-enabled duty-free trade within North America, has translated into the emergence of medical device manufacturing clusters in both countries. (“Clusters” refers to the geographic concentration of interconnected entities in a given industry. In Mexico, clusters are referred to as “maquiladoras.”) Mexico’s largest cluster associated with medical goods production is in Baja California—a region that borders California—which boasts nearly 70 medical device manufacturing facilities, many of which are owned by leading U.S.-led firms, such as CareFusion, DJO Global, Hill-Rom/Welch-Allyn, Integer, and Medtronic. For example, of the $8.3 billion of announced foreign direct investments into Mexico’s medical device sector during 2003–16, U.S. firms represented more than half ($4.5 billion).

Although most of the activity that occurs in Baja California is assembly and relatively low-value activity, evidence suggests that production in this region has been climbing the value chain of production. For example, in Tijuana, where 30 of the 44 facilities operating are owned by U.S. firms, exports of high-value-added goods to the U.S.—including diagnostic and orthopedic equipment—have increased by nearly 50 percent since 2011, according to Global Trade Atlas.

In the U.S., medical goods manufacturing clusters can be found in Massachusetts, Michigan, Minnesota, Indiana, Tennessee, and California. However, bilateral medical goods trade between the U.S. and Mexico is principally driven by the close collaboration between clusters operating in San Diego, Calif., and in Baja California. For example, firms in San Diego accounted for nearly one-half of U.S. medical device imports from Mexico in 2016. At the same time, Baja California-based companies accounted for nearly one-quarter of Mexico’s medical device imports from the U.S. in 2016, according to Global Trade Atlas.

4. Canada has principally served as a leading market for U.S.-finished medical devices.

Canada ranks among the world’s top 10 leading medical goods markets and is heavily dependent on imports, the majority of which is supplied by the U.S. Unlike in Mexico, Canada boasts a relatively mature market for medical goods and has a strong need for high-end medical technologies. Although Canada is boosting its domestic production, as evidenced by manufacturing clusters in Ontario and Quebec—where some 80 percent of the country’s production is located—and substantial investments from leading U.S. firms like Abbott Laboratories, Baxter, GE Healthcare, Philips HealthTech, and Zimmer Biomet. However, in the near term, the country will likely remain a much more significant consumer of medical devices within North America than a supplier. In particular, the U.S. supplied nearly half of Canada’s market during 2016 (as noted in Figure 1), which represented the United States’ fifth largest medical device export market and a leading consumer of high-value-added medical products from the U.S. For example, Canada was a top five recipient of U.S. medical device exports, ranging from orthopedic devices to intravenous diagnostic equipment to diagnostic technologies during 2016.

Mihir Torsekar covers trade and competitiveness issues affecting the U.S. and global medical device industry as part of his duties at the United States International Trade Commission.

Since NAFTA’s inception, total trade in medical products between the U.S. and its NAFTA partners has expanded by nearly 760 percent, reaching $16.5 billion in 2016—eclipsing the growth rate observed between the U.S. and other key markets such as the European Union or East Asia, as well as the rest of the world over the 22-year period. The bulk of regional trade consists of surgical instruments (40 percent); disposable goods, such as hospital supplies (24 percent); and therapeutic devices, such as orthopedic devices, hearing aids, and pacemakers (19 percent).

NAFTA has also facilitated increased trade in industries related to the medical goods manufacturing industry. For example, the U.S. plastics industry claimed to have tallied $29.7 billion in exports to Canada and Mexico during 2016—nearly half of all U.S. plastics exports for the year. Plastics are commonly used for manufacturing devices ranging from surgical instruments to components used in diagnostic technologies.

Figure 1: In 2016, the United States was by far the single largest supplier of medical devices to Canada and Mexico, while Mexico was the largest source of medical devices for the United States (% share). [Source: Compiled by author from IHS Markit, Global Trade Atlas (accessed September 2017).]

Each country in the pact has played a distinct role in this trade story: Mexico has served as an attractive destination for U.S. medical product manufacturers to locate low-cost, less-sophisticated elements of its supply chain; the U.S. has been the region’s predominant supplier of high-end equipment, such as diagnostic technologies, as well as the region’s largest consuming market for medical goods (Figure 1); and Canada, while not as sizeable a market as the U.S., has played a critical role in importing much of the United States’ high-end technologies, such as orthopedic devices, intravenous diagnostic equipment, and various diagnostic technologies. Following is a summary of the four key takeaways from NAFTA.

1. The U.S. trade deficit with its NAFTA partners has increased in recent years.

A stated objective of Robert Lighthizer, the U.S. Trade Representative, has been to reduce the U.S. trade deficit with NAFTA partners. Notably, medical goods manufacturing is one of the few industries in the U.S. that regularly maintains a trade surplus with its global trading partners. In the early years after NAFTA’s inception, the U.S. maintained this trend with its regional trading partners, due primarily to robust Canadian imports of surgical equipment, implantable devices, and intravenous diagnostic equipment from the U.S. However, this trend has reversed in recent years; every year since 2014, the U.S. has witnessed a widening trade deficit for medical goods, which reached $1 billion in 2016 (Figure 2). This development has reflected slightly reduced imports of medical goods into Canada’s maturing medical device market. At the same time, the U.S. bilateral trade deficit with Mexico has remained consistent, driven largely by U.S. imports of surgical equipment from Mexico.

Figure 2: The U.S.-NAFTA trade deficit for medical devices has been increasing since 2014 (billion $). [Source: Compiled by author from IHS Markit, Global Trade Atlas (accessed September 2017).]

2. U.S.-Mexico medical products trade is driven by parts and low-value-added goods.

More than two-thirds of North American medical goods trade is attributable to bilateral trade between Mexico and the U.S. As of 2016, Mexico has emerged as the United States’ largest trading partner of these products. Total trade between these countries principally consists of parts—such as plastic components for intravenous drug delivery catheters; steel used for orthopedic implants; and electronic components used for devices ranging from pacemakers to diagnostic equipment—that are used for manufacturing finished equipment in the U.S.; surgical equipment; and basic hospital supplies, such as first aid kits and surgical gloves.

Of particular note is the United States’ heavy reliance on Mexico to supply parts that are used in the eventual production of finished goods. For example, over the past decade, Mexico has accounted for more than half of the United States’ imports of parts for cardiac pacemakers. Overall, Mexico has been the largest source of U.S. medical goods imports since 2009.

Since NAFTA’s passage, U.S. firms have relocated much of their labor-intensive manufacturing activities to Mexico in an attempt to take advantage of the country’s relatively low labor costs; nearly 90 percent of U.S. investments into Mexico’s medical device sector were directed toward manufacturing during 2003–16. Further, wages for medical device technicians in Tijuana—Mexico’s largest medical device producing city—are roughly 44 percent less than similar jobs in the U.S. according to the New York Times. In contrast, most of the high-value added activities, such as research and development, are largely conducted in the U.S.

3. Medical device clusters in Mexico and the U.S. have driven total regional trade.

Mexico’s proximity to the U.S.—the world’s largest medical device market—coupled with NAFTA-enabled duty-free trade within North America, has translated into the emergence of medical device manufacturing clusters in both countries. (“Clusters” refers to the geographic concentration of interconnected entities in a given industry. In Mexico, clusters are referred to as “maquiladoras.”) Mexico’s largest cluster associated with medical goods production is in Baja California—a region that borders California—which boasts nearly 70 medical device manufacturing facilities, many of which are owned by leading U.S.-led firms, such as CareFusion, DJO Global, Hill-Rom/Welch-Allyn, Integer, and Medtronic. For example, of the $8.3 billion of announced foreign direct investments into Mexico’s medical device sector during 2003–16, U.S. firms represented more than half ($4.5 billion).

Although most of the activity that occurs in Baja California is assembly and relatively low-value activity, evidence suggests that production in this region has been climbing the value chain of production. For example, in Tijuana, where 30 of the 44 facilities operating are owned by U.S. firms, exports of high-value-added goods to the U.S.—including diagnostic and orthopedic equipment—have increased by nearly 50 percent since 2011, according to Global Trade Atlas.

In the U.S., medical goods manufacturing clusters can be found in Massachusetts, Michigan, Minnesota, Indiana, Tennessee, and California. However, bilateral medical goods trade between the U.S. and Mexico is principally driven by the close collaboration between clusters operating in San Diego, Calif., and in Baja California. For example, firms in San Diego accounted for nearly one-half of U.S. medical device imports from Mexico in 2016. At the same time, Baja California-based companies accounted for nearly one-quarter of Mexico’s medical device imports from the U.S. in 2016, according to Global Trade Atlas.

4. Canada has principally served as a leading market for U.S.-finished medical devices.

Canada ranks among the world’s top 10 leading medical goods markets and is heavily dependent on imports, the majority of which is supplied by the U.S. Unlike in Mexico, Canada boasts a relatively mature market for medical goods and has a strong need for high-end medical technologies. Although Canada is boosting its domestic production, as evidenced by manufacturing clusters in Ontario and Quebec—where some 80 percent of the country’s production is located—and substantial investments from leading U.S. firms like Abbott Laboratories, Baxter, GE Healthcare, Philips HealthTech, and Zimmer Biomet. However, in the near term, the country will likely remain a much more significant consumer of medical devices within North America than a supplier. In particular, the U.S. supplied nearly half of Canada’s market during 2016 (as noted in Figure 1), which represented the United States’ fifth largest medical device export market and a leading consumer of high-value-added medical products from the U.S. For example, Canada was a top five recipient of U.S. medical device exports, ranging from orthopedic devices to intravenous diagnostic equipment to diagnostic technologies during 2016.

Mihir Torsekar covers trade and competitiveness issues affecting the U.S. and global medical device industry as part of his duties at the United States International Trade Commission.