Ben Dunn, Managing Director, Covington Associates05.01.17

One of the most concerning aspects of the recent financial boom has been the lack of funding for medical device companies. While the implications of this shortage of capital have an immediate impact on anyone involved in the medical device industry, the shortage will eventually affect our entire society due to our dependence on medical devices that enhance the quality of life. As with most problems, the dearth in funding has been driven by various factors, rather than one single cause.

Taunted by the proclamations of record amounts of available investor capital and cash on company balance sheets, medical device companies of all sizes seeking investments have found it difficult to leverage such financing. With numerous reports about large amounts of available capital and investors’ struggle to put that money to work, the medical device entrepreneur must feel like he or she exists in a parallel universe, because none of the capital has trickled down. Whether it is a Series A or dreaded Series B round—which some refer to as the “valley of death”—it has been difficult to get an investor’s attention, let alone to convince them to part with their money. These obstacles expose more troubling and far-reaching issues within the medtech industry, namely, the amount of money available to companies and the reasons funding has become so difficult to obtain.

Unlike in past years, there is a record amount of capital currently available for investment. According to Bain & Company, there was more than $1.4 trillion of committed but undeployed capital in private equity funds at the end of 2016, and that number doesn’t even include the large amounts of capital controlled by family offices or government investment arms.

Moreover, the National Venture Capital Association reports that healthcare-focused venture capital funds raised over $12 billion of new capital in 2016. Clearly, there is a tremendous amount of dry powder for investment.

So where is the money going?

Certainly not into medical devices. The different investor classes—private equity, venture capital, and corporate investors—are funneling dollars into non-medtech sectors. Private equity firms have focused their investments on more mature businesses with stable cash flows and historical earnings (the opposite of a typical device company profile) while venture capital firms, which back early-stage companies, have invested heavily in non-medical technology organizations. The firms that have remained in healthcare have gravitated to biotechnology companies and ignored the medical device sector. Corporate investors, flush with cash and demonstrating a more risk averse strategy, have focused their efforts on less risky acquisitions rather than making investments in young companies. Rather than take the risk of investing in an early-stage business, OEMs are content to wait for a company to develop and ultimately pay more to acquire the business.

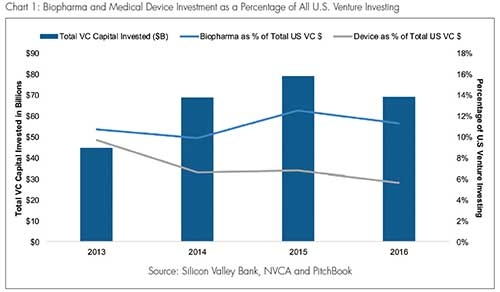

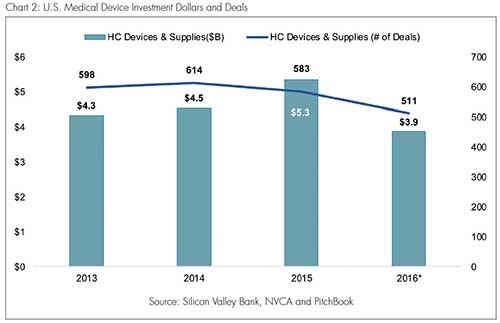

Charts 1 and 2 (based on data compiled by Silicon Valley Bank) show the decline in medical device financing as a percentage of total venture investments. In 2016, of the approximately $75 billion of venture capital invested, just over 5 percent went to medical device companies. That figure represents a relative decrease of more than 50 percent compared with 2010, when over 11 percent of venture investments went toward medical devices. The impact of this relative decline is evident upon a closer examination of 2016, a year in which the aggregate amount of medical device investment dropped by 25 percent (from 2015) to $3.9 billion and the number of investments fell to a five-year low at 511.

There are several reasons for this abscondence from medical devices. The most fundamental explanation involves the principal of risk versus return. Investors prefer financial prospects that give them the greatest chance of returns with the least amount of risk. When compared to other sectors, capitalists consider medical device investments as less attractive on the risk versus return scale. The environment for new medical devices has become much more challenging in recent years. U.S. Food and Drug Administration (FDA) approvals have been less predictable and more time-consuming. Consequently, the longer regulatory process increases time to market and reduces an investor’s time-based rate of return. Even after successfully navigating the FDA gauntlet, medical device companies are not out of the woods yet, as reimbursement has become much more uncertain and tedious. Investors used to be confident about product marketability upon regulatory approval, but that strategy is no longer viable. Regulatory approval is not enough to guarantee success—the device must now also demonstrate that it will be reimbursed and support value-based healthcare initiatives.

Not surprisingly, the liquidity path for medical device companies has become much more difficult as well. The initial public offering (IPO) window has been only open a crack (with a limited number of companies going public), forcing investors to rely on an M&A exit for their liquidity. And while medtech M&A remains very active, there have been some unfavorable changes in recent years affecting investments. Perhaps the most troubling change is the challenging regulatory environment, which has increased the amount of time it takes for an acquisition to occur. Previously, an acquisition would quickly follow regulatory approval; now companies wait to determine the type of market traction for a product (due to reimbursement concerns) before merging. Accordingly, the longer time frame makes an investment less valuable and increases its risk.

Another factor significantly impacting medtech financing is the consolidation among large medical device OEMs. These unions are reducing the number of potential buyers of businesses, leaving investors with fewer exit options and lower values. Medical device exits for VC-backed companies hit a three-year low in 2016, with the industry experiencing only three IPOs and 13 M&A transactions, according to Silicon Valley Bank. Exits for device companies are taking longer and occurring increasingly in later stages. Over the past three years, two-thirds of the companies with meaningful exits have been commercial stage while only 18 percent have been pre-approval stage, thereby increasing the average time to exit for medical device companies to more than eight years in 2016.

The industry’s financial struggles become even more troubling when compared with the glut of biotechnology investments. As medical device companies fight to attract funding, biotechnology firms have attracted record amounts of funding seemingly with ease. Since 2010, annual investments in biotechnology have more than doubled, from less than $4 billion annually to just under $9 billion. While this disparity certainly is frustrating to medtech entrepreneurs, there are some important factors that have made the biotechnology sector more appealing. First and foremost, biotechnology has produced several impressive exits for investors. It almost seems as if an early-stage biotechnology company is being acquired on a weekly basis. There has also been a steady stream of IPOs providing both liquidity for investors and new potential buyers for startups. Finally, biotechnology firms are striking deals earlier in their lifecycle. Investors don’t even wait for regulatory approval anymore—phase 2 clinical results are often sufficient for buyers. An evaluation of large biotechnology exits over the past two years shows that more than half of the major exits occurred in companies that were either in the pre-clinical stage or had just completed phase I trials. Considering most medical device exits occurred after eight years and well into commercialization, it is easy to understand the allure of the biotechnology sector.

A Light at the End of the Tunnel?

Those of us who have lived through a number of business cycles know the investment pendulum will eventually swing back to medical devices. The long-term fundamentals of this market remain too strong and the global need too great for investors to ignore. Sooner or later, the sectors currently in favor will begin to overheat, burning stakeholders and forcing them to seek new investment areas. Intrepid and contrarian financiers who anticipate this shift will reap the greatest rewards, as they will realize there are great returns awaiting in the medical device space. The lack of recent funding has left fewer startups with which to compete, increasing companies’ chances of success. In time, healthcare investors will naturally start to look for alternatives to informatics and biotechnology ventures, and when they change their focus, they’ll find a new breed of medical device startups. In this class will be companies that have developed capital-efficient models through the effective use of outsourced partners. These companies will also be managed by executives who take nothing for granted and understand their products must provide better clinical efficacy as well as greater societal value.

Cause for optimism can be found upon closer evaluation of medical device investments last year. Series A investments reached a 10-year high of 60 companies in 2016, nearly doubling from the previous year’s total. This shift could potentially indicate that institutional investors may be looking more closely at medical device companies and are planting more seeds. One can only hope that investors will continue to nurture these promising young companies and not let them wither on the vine.

Ben Dunn is a managing director with Boston, Mass.-based Covington Associates. For more than 20 years, he has advised medical technology companies in the areas of mergers, acquisitions, investments, and strategic partnerships. Having advised clients on more than 100 transactions, Dunn has represented both private and public companies on both the buy and sell side. He is a frequent speaker at healthcare conferences and the author of numerous articles, including the whitepaper, “Medical Device Outsourcing Industry: Emerging Trends and Opportunities.”

Taunted by the proclamations of record amounts of available investor capital and cash on company balance sheets, medical device companies of all sizes seeking investments have found it difficult to leverage such financing. With numerous reports about large amounts of available capital and investors’ struggle to put that money to work, the medical device entrepreneur must feel like he or she exists in a parallel universe, because none of the capital has trickled down. Whether it is a Series A or dreaded Series B round—which some refer to as the “valley of death”—it has been difficult to get an investor’s attention, let alone to convince them to part with their money. These obstacles expose more troubling and far-reaching issues within the medtech industry, namely, the amount of money available to companies and the reasons funding has become so difficult to obtain.

Unlike in past years, there is a record amount of capital currently available for investment. According to Bain & Company, there was more than $1.4 trillion of committed but undeployed capital in private equity funds at the end of 2016, and that number doesn’t even include the large amounts of capital controlled by family offices or government investment arms.

Moreover, the National Venture Capital Association reports that healthcare-focused venture capital funds raised over $12 billion of new capital in 2016. Clearly, there is a tremendous amount of dry powder for investment.

So where is the money going?

Certainly not into medical devices. The different investor classes—private equity, venture capital, and corporate investors—are funneling dollars into non-medtech sectors. Private equity firms have focused their investments on more mature businesses with stable cash flows and historical earnings (the opposite of a typical device company profile) while venture capital firms, which back early-stage companies, have invested heavily in non-medical technology organizations. The firms that have remained in healthcare have gravitated to biotechnology companies and ignored the medical device sector. Corporate investors, flush with cash and demonstrating a more risk averse strategy, have focused their efforts on less risky acquisitions rather than making investments in young companies. Rather than take the risk of investing in an early-stage business, OEMs are content to wait for a company to develop and ultimately pay more to acquire the business.

Charts 1 and 2 (based on data compiled by Silicon Valley Bank) show the decline in medical device financing as a percentage of total venture investments. In 2016, of the approximately $75 billion of venture capital invested, just over 5 percent went to medical device companies. That figure represents a relative decrease of more than 50 percent compared with 2010, when over 11 percent of venture investments went toward medical devices. The impact of this relative decline is evident upon a closer examination of 2016, a year in which the aggregate amount of medical device investment dropped by 25 percent (from 2015) to $3.9 billion and the number of investments fell to a five-year low at 511.

There are several reasons for this abscondence from medical devices. The most fundamental explanation involves the principal of risk versus return. Investors prefer financial prospects that give them the greatest chance of returns with the least amount of risk. When compared to other sectors, capitalists consider medical device investments as less attractive on the risk versus return scale. The environment for new medical devices has become much more challenging in recent years. U.S. Food and Drug Administration (FDA) approvals have been less predictable and more time-consuming. Consequently, the longer regulatory process increases time to market and reduces an investor’s time-based rate of return. Even after successfully navigating the FDA gauntlet, medical device companies are not out of the woods yet, as reimbursement has become much more uncertain and tedious. Investors used to be confident about product marketability upon regulatory approval, but that strategy is no longer viable. Regulatory approval is not enough to guarantee success—the device must now also demonstrate that it will be reimbursed and support value-based healthcare initiatives.

Not surprisingly, the liquidity path for medical device companies has become much more difficult as well. The initial public offering (IPO) window has been only open a crack (with a limited number of companies going public), forcing investors to rely on an M&A exit for their liquidity. And while medtech M&A remains very active, there have been some unfavorable changes in recent years affecting investments. Perhaps the most troubling change is the challenging regulatory environment, which has increased the amount of time it takes for an acquisition to occur. Previously, an acquisition would quickly follow regulatory approval; now companies wait to determine the type of market traction for a product (due to reimbursement concerns) before merging. Accordingly, the longer time frame makes an investment less valuable and increases its risk.

Another factor significantly impacting medtech financing is the consolidation among large medical device OEMs. These unions are reducing the number of potential buyers of businesses, leaving investors with fewer exit options and lower values. Medical device exits for VC-backed companies hit a three-year low in 2016, with the industry experiencing only three IPOs and 13 M&A transactions, according to Silicon Valley Bank. Exits for device companies are taking longer and occurring increasingly in later stages. Over the past three years, two-thirds of the companies with meaningful exits have been commercial stage while only 18 percent have been pre-approval stage, thereby increasing the average time to exit for medical device companies to more than eight years in 2016.

The industry’s financial struggles become even more troubling when compared with the glut of biotechnology investments. As medical device companies fight to attract funding, biotechnology firms have attracted record amounts of funding seemingly with ease. Since 2010, annual investments in biotechnology have more than doubled, from less than $4 billion annually to just under $9 billion. While this disparity certainly is frustrating to medtech entrepreneurs, there are some important factors that have made the biotechnology sector more appealing. First and foremost, biotechnology has produced several impressive exits for investors. It almost seems as if an early-stage biotechnology company is being acquired on a weekly basis. There has also been a steady stream of IPOs providing both liquidity for investors and new potential buyers for startups. Finally, biotechnology firms are striking deals earlier in their lifecycle. Investors don’t even wait for regulatory approval anymore—phase 2 clinical results are often sufficient for buyers. An evaluation of large biotechnology exits over the past two years shows that more than half of the major exits occurred in companies that were either in the pre-clinical stage or had just completed phase I trials. Considering most medical device exits occurred after eight years and well into commercialization, it is easy to understand the allure of the biotechnology sector.

A Light at the End of the Tunnel?

Those of us who have lived through a number of business cycles know the investment pendulum will eventually swing back to medical devices. The long-term fundamentals of this market remain too strong and the global need too great for investors to ignore. Sooner or later, the sectors currently in favor will begin to overheat, burning stakeholders and forcing them to seek new investment areas. Intrepid and contrarian financiers who anticipate this shift will reap the greatest rewards, as they will realize there are great returns awaiting in the medical device space. The lack of recent funding has left fewer startups with which to compete, increasing companies’ chances of success. In time, healthcare investors will naturally start to look for alternatives to informatics and biotechnology ventures, and when they change their focus, they’ll find a new breed of medical device startups. In this class will be companies that have developed capital-efficient models through the effective use of outsourced partners. These companies will also be managed by executives who take nothing for granted and understand their products must provide better clinical efficacy as well as greater societal value.

Cause for optimism can be found upon closer evaluation of medical device investments last year. Series A investments reached a 10-year high of 60 companies in 2016, nearly doubling from the previous year’s total. This shift could potentially indicate that institutional investors may be looking more closely at medical device companies and are planting more seeds. One can only hope that investors will continue to nurture these promising young companies and not let them wither on the vine.

Ben Dunn is a managing director with Boston, Mass.-based Covington Associates. For more than 20 years, he has advised medical technology companies in the areas of mergers, acquisitions, investments, and strategic partnerships. Having advised clients on more than 100 transactions, Dunn has represented both private and public companies on both the buy and sell side. He is a frequent speaker at healthcare conferences and the author of numerous articles, including the whitepaper, “Medical Device Outsourcing Industry: Emerging Trends and Opportunities.”