SImon Trinh, Senior Research Analyst; Jeffrey Wong, Analyst Director;, iData Research12.03.18

Due to the emergence of advanced diagnostic and imaging technology for the operating room (OR), operating spaces are becoming increasingly congested and complex with a multitude of OR devices and monitors. As a result, ORs are becoming more ergonomically designed and purposefully built with systems that increase efficiency in order to reduce procedure time and improve surgery success rates.

These ORs, known as integrated and hybrid ORs, utilize the most advanced video systems, digital image capture devices, integration hubs/routers/racks, and other capital equipment used in the medical industry. Massive growth in OR equipment is driving the excitement of upgrading to 4K resolution in surgical displays and cameras.

Advanced Imaging and Video Systems

Hybrid ORs incorporate imaging technology like computed tomography (CT), magnetic resonance (MR), and C-arm X-ray systems to assist surgeons in performing quicker, more successful surgeries. By bringing imaging into or adjacent to the surgical space, patients don’t have to be moved during and between surgery, reducing risk and inconvenience. Hybrid ORs require a high investment cost, due to the integration of some of the most advanced imaging and video systems available in the medical device market. Currently, all the hype surrounds 4K devices, with a horizontal screen display resolution of approximately 4,000 pixels. In the healthcare industry, 4096 × 2160 (DCI 4K) is considered the “full 4K” resolution, although many companies still offer UHD displays, which have a resolution just slightly lower than 4K (3840 x 2160 pixels).

High Anticipated Growth, Particularly in China

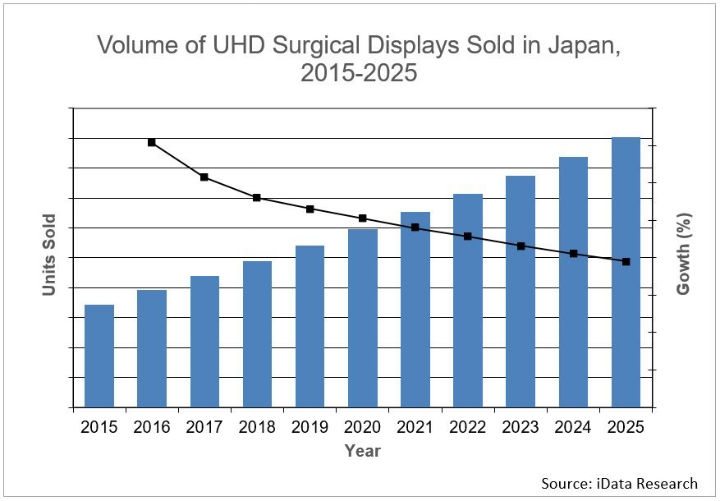

4K devices are expected to experience moderate to high growth in most countries around the world. In Japan, UHD surgical displays have been available and the market has been growing for the last several years at low double-digit rates. 4K surgical displays are available in Japan, but not as widely used compared to UHD displays. Although a growing percentage of facilities have converted to UHD and 4K, there is still a considerable HD installed base in both Japan and China. The conversion of this installed base will continue to drive growth in the number of units sold in the market.

4K surgical cameras, on the other hand, are newer to the market and the market has been experiencing double-digit growth rates. Surgical camera systems are used primarily in minimally invasive surgeries (MIS). MIS procedures result in faster recovery time, fewer infections, and significant overall savings compared to open surgeries. For these reasons and more, hospitals are willing to invest a significantly higher amount on upgrading HD devices to a much higher quality 4K device. Over the next seven years, the market for 4K surgical cameras in Japan is expected to continue significant growth.

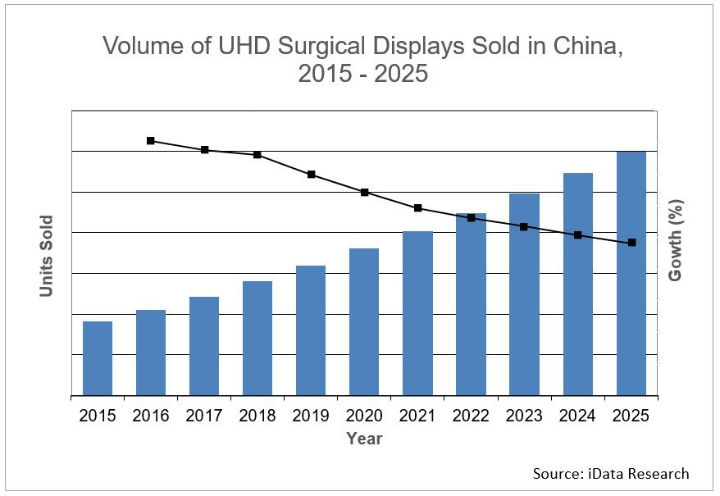

In China, due to their slow regulatory and approval process, 4K cameras did not receive official approval and no devices were sold until 2018. However, in early 2018, the Chinese government officially allowed sales of 4K camera systems, granting permission to several companies including Arthrex, Olympus, and Richard Wolf. However, UHD surgical displays were already sold in China and were quickly gaining popularity among hospitals, with sales volume growing at rates in the mid-teens. Over the next seven years, the market for UHD displays is expected to continue double-digit growth, while the market for 4K cameras is expected to take off and exhibit growth rates in the high teens as well.

Leading Competitors

In Japan, the leading competitors for 4K camera devices are Olympus, Arthrex, and Richard Wolf. Olympus released the VISERA 4K UHD camera system in 2015, making it one of only three major companies that offer a 4K camera system. In late 2014, Arthrex released the SynergyUHD4 4K camera system, which was the world’s first 4K camera on the market. The continued success of the SynergyHD3 camera system and the introduction of the first 4K camera has fostered high brand recognition for Arthrex. In 2017, Richard Wolf released its ENDOCAM Logic 4K surgical camera heads and CCUs into the market. This 4K platform can be used efficiently in all endoscopic specialties and can be incorporated within operating room integration systems like Richard Wolf’s core nova.

For the surgical display markets, Olympus, EIZO, and Barco were the main competitors in both Japan and China. Olympus entered the display market through a partnership with SONY which enabled the company to offer a 4K UHD system. On June 6, 2016, EIZO acquired Panasonic Healthcare Co., Ltd.'s endoscopy monitor business. This acquisition provides EIZO with a complete lineup of endoscopy monitors including 3D and 4K. Barco offers the MDSC line of surgical displays, which come in sizes ranging from 19” to 58”. Its 58” Quad UHD MDSC-8258 display was designed specifically for hybrid ORs and features multi-modality imaging and 3,840 x 2,160-pixel density.

Market Insights

As adoption rates for 4K devices begin to rise, one of the greatest limiters of growth will be the entrance of new competitors, particularly Asian manufacturers offering lower-priced products. This does not necessarily force established players to reduce prices, but it does lower the average price, particularly in countries like China where these low-priced products are gaining market share. However, top-tiered hospitals understand that 4K camera systems carry a higher cost than their HD counterparts, and are willing to pay a higher price to ensure top-quality product for critical, life-or-death procedures.

References

China Market Report Suite for Video and Integrated Operating Room Equipment 2019 – MedSuite, iData Research

Japan Market Report Suite for Video and Integrated Operating Room Equipment 2019 – MedSuite, iData Research

Simon Trinh is a senior research analyst at iData Research, with many years of experience researching the Asia-Pacific and European markets and was the lead researcher on the study mentioned in this article on operating room equipment.

Jeffrey Wong is the analyst director at iData Research. Through many years of analysis, he has been the lead on most of iData’s medical, dental, and pharmaceutical market research and now drives research strategy, product development, and consulting research.

These ORs, known as integrated and hybrid ORs, utilize the most advanced video systems, digital image capture devices, integration hubs/routers/racks, and other capital equipment used in the medical industry. Massive growth in OR equipment is driving the excitement of upgrading to 4K resolution in surgical displays and cameras.

Advanced Imaging and Video Systems

Hybrid ORs incorporate imaging technology like computed tomography (CT), magnetic resonance (MR), and C-arm X-ray systems to assist surgeons in performing quicker, more successful surgeries. By bringing imaging into or adjacent to the surgical space, patients don’t have to be moved during and between surgery, reducing risk and inconvenience. Hybrid ORs require a high investment cost, due to the integration of some of the most advanced imaging and video systems available in the medical device market. Currently, all the hype surrounds 4K devices, with a horizontal screen display resolution of approximately 4,000 pixels. In the healthcare industry, 4096 × 2160 (DCI 4K) is considered the “full 4K” resolution, although many companies still offer UHD displays, which have a resolution just slightly lower than 4K (3840 x 2160 pixels).

High Anticipated Growth, Particularly in China

4K devices are expected to experience moderate to high growth in most countries around the world. In Japan, UHD surgical displays have been available and the market has been growing for the last several years at low double-digit rates. 4K surgical displays are available in Japan, but not as widely used compared to UHD displays. Although a growing percentage of facilities have converted to UHD and 4K, there is still a considerable HD installed base in both Japan and China. The conversion of this installed base will continue to drive growth in the number of units sold in the market.

4K surgical cameras, on the other hand, are newer to the market and the market has been experiencing double-digit growth rates. Surgical camera systems are used primarily in minimally invasive surgeries (MIS). MIS procedures result in faster recovery time, fewer infections, and significant overall savings compared to open surgeries. For these reasons and more, hospitals are willing to invest a significantly higher amount on upgrading HD devices to a much higher quality 4K device. Over the next seven years, the market for 4K surgical cameras in Japan is expected to continue significant growth.

In China, due to their slow regulatory and approval process, 4K cameras did not receive official approval and no devices were sold until 2018. However, in early 2018, the Chinese government officially allowed sales of 4K camera systems, granting permission to several companies including Arthrex, Olympus, and Richard Wolf. However, UHD surgical displays were already sold in China and were quickly gaining popularity among hospitals, with sales volume growing at rates in the mid-teens. Over the next seven years, the market for UHD displays is expected to continue double-digit growth, while the market for 4K cameras is expected to take off and exhibit growth rates in the high teens as well.

Leading Competitors

In Japan, the leading competitors for 4K camera devices are Olympus, Arthrex, and Richard Wolf. Olympus released the VISERA 4K UHD camera system in 2015, making it one of only three major companies that offer a 4K camera system. In late 2014, Arthrex released the SynergyUHD4 4K camera system, which was the world’s first 4K camera on the market. The continued success of the SynergyHD3 camera system and the introduction of the first 4K camera has fostered high brand recognition for Arthrex. In 2017, Richard Wolf released its ENDOCAM Logic 4K surgical camera heads and CCUs into the market. This 4K platform can be used efficiently in all endoscopic specialties and can be incorporated within operating room integration systems like Richard Wolf’s core nova.

For the surgical display markets, Olympus, EIZO, and Barco were the main competitors in both Japan and China. Olympus entered the display market through a partnership with SONY which enabled the company to offer a 4K UHD system. On June 6, 2016, EIZO acquired Panasonic Healthcare Co., Ltd.'s endoscopy monitor business. This acquisition provides EIZO with a complete lineup of endoscopy monitors including 3D and 4K. Barco offers the MDSC line of surgical displays, which come in sizes ranging from 19” to 58”. Its 58” Quad UHD MDSC-8258 display was designed specifically for hybrid ORs and features multi-modality imaging and 3,840 x 2,160-pixel density.

Market Insights

As adoption rates for 4K devices begin to rise, one of the greatest limiters of growth will be the entrance of new competitors, particularly Asian manufacturers offering lower-priced products. This does not necessarily force established players to reduce prices, but it does lower the average price, particularly in countries like China where these low-priced products are gaining market share. However, top-tiered hospitals understand that 4K camera systems carry a higher cost than their HD counterparts, and are willing to pay a higher price to ensure top-quality product for critical, life-or-death procedures.

References

China Market Report Suite for Video and Integrated Operating Room Equipment 2019 – MedSuite, iData Research

Japan Market Report Suite for Video and Integrated Operating Room Equipment 2019 – MedSuite, iData Research

Simon Trinh is a senior research analyst at iData Research, with many years of experience researching the Asia-Pacific and European markets and was the lead researcher on the study mentioned in this article on operating room equipment.

Jeffrey Wong is the analyst director at iData Research. Through many years of analysis, he has been the lead on most of iData’s medical, dental, and pharmaceutical market research and now drives research strategy, product development, and consulting research.