Jennifer Whitney04.12.07

A Clear Picture

Top Imaging Companies Share Their Perspectives on Industry Advancements and What’s to Come

Jennifer Whitney

Editor

At some point in life, chances are good that you will undergo some type of imaging procedure to help pinpoint the source of a problem within your body. Whether the modality is magnetic resonance (MR), computed tomography (CT), ultrasound or even X-ray—or some combination of these types of technology—usually the procedure isn’t painful because it’s not invasive. That doesn’t mean it can’t induce nerve-wracking fear, though.

For this reason, anything that can be completed as quickly as possible may help patients relax a bit sooner. Even more important, the clinical benefits derived from the latest scanning technology on the market are helping to change the way medicine is practiced.

The GEMINI TF PET/CT scanner (shown above) is a prime example of where imaging is headed in the future. Imaging equipment that combines modalities, especially as molecular imaging grows, is expected to transform medicine over the next decade. Photo courtesy of Philips Medical Systems North America. |

“That may not seem significant now, but if you think about it, as we get older we get more obese and sicker,” explained Desch, noting the additional benefits of advances in imaging. “You have to hold your breath during that type of procedure, so if you could have the person lay on the table and only do so that long, it’s great for everyone involved.”

The medical community has spent many years looking at best practices for shifting disease management from diagnosis and treatment to prevention. Common sense dictates that when problems are detected and diagnosed at an early stage, more treatment options are available. Therefore, manufacturers of imaging technology are optimizing next-generation equipment with capabilities that will allow healthcare professionals not just to see a picture of what’s going on in the body, but also visualize metabolic activity and blood flow, among other functions, and combine data with knowledge to see the big picture.

Countless other benefits of today’s imaging modalities are evident, based on what the market has seen unveiled in the past few years and by what’s in the R&D pipeline. Efficiency is unparalleled, given the tremendous improvements seen in resolution, computer power, detection sensitivity and even the smaller size of the equipment. Along with these strides, manufacturers have managed to produce modalities that use lower amounts of radiation.

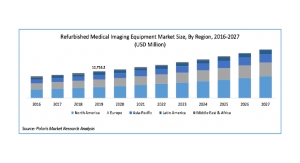

Note: All figures are rounded; the base year is 2000. Figure reproduced with permission from Frost & Sullivan. The figure originally was published in the report, “U.S. Medical Imaging Markets.” For more information about this report or to purchase a copy of it, please visit www.frost.com. |

Digitizing Imaging

One of the biggest shifts occurring at present is the conversion from analog to digital systems, as well as the growth of ancillary IT support products that work in tandem with imaging equipment.

“Imaging technology has been growing by leaps and bounds in almost direct proportion to advances in the computer industry,” said Joseph Camaratta Jr., vice president, global solutions for Siemens Medical Solutions in Malvern, PA. “As that industry engineers faster processors, we can leverage that technology to improve medical imaging devices. Improvements in processing technology allow us to provide ways of quickly handling large amounts of data. Delivering detailed images is just half the story. Healthcare providers also need a way to quickly manipulate those images to make a timely diagnosis…[and] they need solutions to store and access those data as necessary.”

Digitalization in the imaging market is growing by 15% to 20% annually, according to Adetola “A.J.” Ajibade, a healthcare research analyst for Frost & Sullivan.

“Most facilities are still using analog systems, but it’s not indicative of what’s going to happen in the future,” he said. Although only about 2,500 digital systems currently are installed in the United States—compared with about 13,000 analog systems—unit shipments for digital imaging equipment outnumber analog equipment by a ratio of five to one, Ajibade said.

Although converting from analog to digital systems initially may be expensive for many institutions, over time a digital system will be more cost effective than analog’s reliance on paper film, experts said. In addition, electronic storage will help hospitals reallocate floor space for more useful purposes.

Most important, however, is the visual advantage that digital readings offer clinicians. For example, mammography, a mainstay in women’s healthcare, is one area that manufacturers believe has especially benefited from the advent of digital technology. When using analog, clinicians typically have to transfer images on film to a scanner and then are limited to static anatomical views. Since digital images are stored electronically, a practitioner has the ability to zoom in or out and tweak an image to spot lesions that may have been missed on a paper film.

The equipment, combined with ancillary IT products, isn’t just about producing images but also enhanced information. If a patient visits the emergency room complaining of chest pain, for example, attendants may perform an EKG, blood work and a CT scan and then feed all the information into a network that would enable a cardiologist to review all findings in context (and in one spot) to make an educated diagnosis within mere hours. This is a far cry from the days of having one procedure after another, only to find the need for an invasive procedure to confirm suspicions.

“‘Exploratory surgery’ are words you don’t hear much anymore in medicine,” said Sean Burke, chief marketing officer, diagnostic imaging business for GE Healthcare in Waukesha, WI. “Technology has become so much more efficient.”

Weighing Cost Against Need

The Senographe Essential is the next generation of GE’s Senographe Full Field Digital Mammography systems. Photo courtesy of GE Healthcare. |

Sales growth won’t be an easy task for any of the industry’s players, though. According to Ajibade, some of the newest units can cost up to $500,000. While busy metropolitan areas and advanced medical research centers may be able to afford the high price, smaller communities often cannot afford to reap the benefits of innovation as quickly. “There’s enough of a base [of customers] out there that the rural places aren’t being considered,” Ajibade claimed. “Are there companies out there that are trying to give incentives to help the facilities acquire the technology? Sure, but by and large [OEMs] calculate what they need to buy and sell, and they set the standard.”

Although the cost of the equipment isn’t a minor investment, the increased productivity offered (eg, faster scan time, more targeted readings) means more of the population could be served as physicians have time to see more patients on a given day, Camaratta said. In addition, manufacturers noted that the newer equipment lasts longer than previous incarnations.

Burke concluded, “All the moves we [at GE in particular] have made have been supportive of our vision: everyone said the healthcare system is broken. It’s incumbent on the industry to articulate the value imaging brings. We have to collect data from clinical trials to communicate the value to stakeholders.”

The value may be evident, but along with the rest of the device community, imaging specialists must contend with tightened purses with insurers and other providers of medical reimbursement. Another thorn in their side is the federal Deficit Reduction Act (DRA), which was implemented on January 1 this year. This legislation is set to cut reimbursement for imaging procedures in non-hospital settings by $3 billion over the next five years, with compensation being reduced by 15%-70% (depending on the type of procedure) compared with last year.

“I don’t want to say the future is ominous, but it’s not bright in this regard,” Ajibade said. “This [DRA] will discourage many doctors from using these procedures. If they’re not performing the procedures, then who is using the modality? As a result, the hospital will then have to think twice about buying the equipment.”

Although this issue may have manufacturers concerned, Ajibade recommends that OEMs can help shape their own future by becoming more politically active and lobbying to have their voice heard by Congress. “The areas that weren’t hit with cuts—such as mammography—had political backing. [Com-panies] need to sponsor programs that will put it out there that these imaging procedures have medical benefits. If payments are too low and doctors aren’t using them, then patients’ lives will be at stake,” he concluded.

Equipment manufacturers say they are ready to respond to the issue. “We certainly support the government effort to keep cost in line and increase productivity in healthcare,” Desch said. “You will see companies produce documentation showing how the imaging technology is saving the healthcare industry money.”

A Competitive Market?

Even as imaging equipment manufacturers strive to save the healthcare industry (and patients) money over time by preventing disease progression, they are pouring many of their profits into R&D programs to come up with even more impressive technology.

The top-ranked (by sales) industry players in this market are in an interesting position, as the type of capital investment needed to bring certain imaging technology to market limits the amount of competition these companies face. GE, for example, spent $100 million over 10 years on R&D for digital detection equipment alone, Ajibade said, and Siemens spent $50 million.

“It’s so hard to get these kinds of products to market and maintain them that it’s hard for a smaller, third-tier player to get in,” he explained.

This may help to explain some of the activity occurring among the larger manufacturers in this space. The smaller companies, realizing they don’t have the capital to invest in some of the equipment that the largest OEMs have, are focusing on niche products or ancillary equipment. Outsourcing partners in this sector also have a better likelihood of sustaining themselves, Ajibade said, because they aren’t in direct competition with their OEM customers.

As with many sectors of the medical device industry, the limited playing field and focus on niche products by smaller companies makes them prime targets for acquisition by the larger players.

In imaging, each of the industry’s largest OEMs maintains its own vision, strategy and path to differentiation. Philips, for example, has been acquiring companies that support the firm’s approach to provide care throughout a patient’s entire lifespan. “Being a company that’s focused on care cycles, we’re acquiring companies that give us the ability to treat from point of disease to home care,” Desch said.

Similarly, Siemens Medical Solutions recently acquired Bayer’s diagnostics division, which now allows the company to combine its imaging capabilities with in vitro laboratory tests on blood serum and in vivo testing of novel biomarkers.

“These biomarkers will serve many roles,” Camaratta explained. “Most importantly, they can help us predict if patients have a specific disease, or if they will progress to a more advanced form of a disease. They also can help us figure out the best therapy to deliver to patients.”

And, of course, GE Healthcare has its own approach. “We’re the most enabled company to combine chemistry, biology and technology,” Burke said, explaining that all of the organization’s acquisitions in the past few years have played into its strategy of identifying problems early on so healthcare can be approached preventatively rather than targeting disease after symptoms have manifested. Acquisitions have included Amersham for biologic and chemistry expertise, as well as IDX Systems Corporation for IT platform integration. In addition, the company is expected to complete its acquisition of Abbott’s diagnostic divisions for IVD capabilities later this spring.

Regardless of the path each company takes, imaging equipment manufacturers are focusing on combining different disciplines to create an all-encompassing, holistic approach to medicine. In leaving no stone unturned, patients and their healthcare providers alike are sure to benefit in times to come.

SIDEBAR - What’s Ahead: A Peek at Some Promising Technology

It’s no easy feat bringing a new product to market today, but the pace of innovation makes it easy to feel optimistic about the future of imaging capabilities. Following is a look at what experts believe are some of the most exciting technologies available now as well as what to expect in the next few years.

In general, visualization ability has come a long way thanks to better resolution and spectrometry. The ability to see in increasing dimensions will enhance a clinician’s ability to truly track what’s going on in the body.

Commenting on the promise of 4-D technology, Sean Burke, chief marketing officer, diagnostic imaging business for GE Healthcare in Waukesha, WI, gave the following example: “If you have lung cancer, every time you breathe, your lung moves. What happens is that the contour of a tumor changes as you breathe. If you are taking a static image, it could change shape as you’re breathing. With 4D, it allows a full view of all the movement of the tumor and additionally allows a view of the contour of that tumor.”

Hybrid equipment is another area of interest. Equipment that combines modalities offers physicians different types of visualization never achieved before and produces innovative treatments for common medical problems. For example, GE Healthcare’s ExAblate 2000 is an MR-guided ultrasound system that offers noninvasive treatment of uterine fibroids by using an ultrasound device to ablate fibroid tumors with the use of targeted heat as the patient rests on an MR table.

John Desch, vice president, marketing and strategy for Philips Medical Systems North America in Andover, MA, said another device commonly being adopted is CT combined with PET (positron emission tomography). Introduced only in the past decade, this technology “marries” anatomical structure with molecular structure. Since CT is capable of showing tissue but not what’s going on within it, the combination of CT and PET offers new frontiers of discovery. The equipment fuses the two types of images together and enables a physician to see both the anatomy and metabolic uptake of an isotope, which enables the professional to see what’s happening in the tissue being examined.

Siemens Medical Solutions offers this technology as well. “PET/CT is recognized as a staging modality for colon cancer [for example],” said Joseph Camaratta Jr., vice president, global solutions for the Malvern, PA-based company. “Combined images from [our] PET/CT scanners can help physicians define how aggressive the disease is and what therapy is the best option.”

The most exciting advances to come in imaging, experts agreed, involve molecular imaging; in fact, each of the top three (in terms of annual sales) imaging manufacturers said it’s a top focus of their R&D efforts. Giving clinicians the ability to monitor cellular activity in the body will transform medicine by enabling professionals to look for disease before symptoms are detected.