Maria Shepherd, President and Founder, Medi-Vantage04.01.22

A growing number of individuals continue to be diagnosed with deep vein thrombosis (DVT) as a result of rising public awareness of the condition, often associated with a chronic obstructive condition. While the majority of patients with venous thromboembolization (VTE) receive anticoagulation to obviate thrombus embolization, up to 20 to 50 percent develop post thrombotic syndrome (PTS). PTS can lead to major disability and poor quality of life, with prominent symptoms including severe and chronic pain and limb swelling.1 The placement of endovenous stents is recognized as an effective means of restoring venous blood flow and preventing recurring DVT.

Why This Is Important

There are other options, however, to treat these conditions. According to Inari executive leadership speaking at the SVB Leerink conference,2 the VTE markets for DVT and pulmonary embolism (PE) treatment can also be treated by mechanical thrombectomy. They believe the markets for DVT and PE remain deeply underpenetrated by VTE interventional technology with approximately 10 percent of PE patients, and a slightly greater percentage of DVT patients, being treated interventionally with mechanical thrombectomy. Analysts from SVBLeerink believe this indicates a large runway remains ahead of Inari and their competitors as they continue to penetrate these markets.2

Interventions in Peripheral Vascular Disease

Also in the peripheral vascular segment, Penumbra—a direct competitor of Inari—reported the U.S. vascular thrombectomy segment growing by 10 percent.3 While Penumbra reported procedural declines from increased rates of COVID-related VTE since the onset, executive management stated this factor doesn’t appear to be significantly affecting their numbers to date. Market development continues to expand technology utilization into a broader range of patients within the venous segment, especially for those traditionally given conservative medical management. Patients with peripheral artery disease (PAD) are at risk for cardiovascular and limb ischemic events, including acute limb ischemia (ALI).4 ALI is characterized by the sudden decrease in limb perfusion that threatens viability of the limb.

Penumbra management indicates that recently launched technology—the Lightning 7 (designed for single session arterial thrombus removal)—has been well received by interventionalists.

Interventions in Neurovascular Disease

Stroke mechanical thrombectomy (SMT) is another large market for thrombectomy devices. In a BTIG 3rd annual survey of the neurovascular device space, SMT adoption saw a slowdown in 2020 due to COVID, but since then, SMT use has grown steadily.5 In the BTIG 2021 survey, they estimated SMT adoption was growing from 2019 through 2021 at a CAGR of ~16 percent, and CAGR would increase to ~17 percent through 2025. BTIG also estimates the serviceable addressable market of ischemic strokes is ~200,000 annually in the U.S., and estimated market share of SMT is ~25 percent. This survey yields interesting results. The field of interventional neurology continues to grow, with 92 percent of interventional neurologists reporting they treat stroke patients versus eight percent of interventional neuroradiologists.

These numbers are important. Several interventionalists in this survey mentioned the increased use of perfusion imaging as a new tool in treating stroke patients. Perfusion imaging uses an intravascular tracer and serial imaging to measure blood flow in the brain.6 In acute ischemic stroke, perfusion imaging may improve diagnostic accuracy, aid treatment target identification, and provide information about functional outcome. In addition, perfusion imaging can recognize which patients may benefit from reperfusion outside the conventional time window or those where the time of symptom onset is unknown.

Using perfusion imaging in the treatment of acute stroke allows personalized treatment of stroke patients based on the condition of their brain tissue, as opposed to traditional time-based treatment.

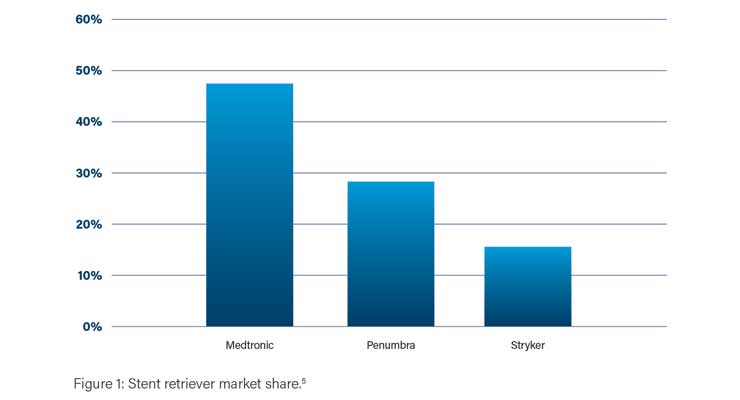

The BTIG survey also estimated stent retriever share was highest for Medtronic, followed by Penumbra and Stryker (Figure 1).5 A new company rapidly gaining market share is Rapid Medical, a private company that launched the Tigertriever in the U.S. in 2Q21. BTIG analysts believe there could be growing use of stent retrievers for deep clots in the brain where the opportunity for aspiration may be restricted.

When asked what percent of your ischemic stroke patients do you treat with SMT (defined as stent retrievers, coil retrievers, or aspiration catheters) and if that percentage of patients treated with SMT will increase or decrease in the next 12 months, respondents signaled an increase in use of SMT from 25 percent in Feb 2022 to 29 percent in February of 2023. When asked about treatment of stroke patients using an SMT direct aspiration first-pass technique (ADAPT), physicians responded that using these types of catheters will increase to 37 percent of all SMT procedures by May 2022 and was expected to further increase to 40 percent of all SMT used. Reasons given were that these catheters were successful 80 percent of the time in removing clots, and this technology was a substantial improvement.5

Respondents are also willing to combine devices if they expect it will improve outcomes. Use of a stent retriever in combination with an aspiration device is a technique called “Solumbra.”7 It has emerged as a popular method of mechanical thrombectomy for acute ischemic stroke. There are multiple variations in the technique, few have been studied, and it is uncertain how these techniques affect patient outcomes. The BTIG respondents estimated the percent of SMT patients treated using Solumbra will rise to 13.9 percent to 14.3 percent.5

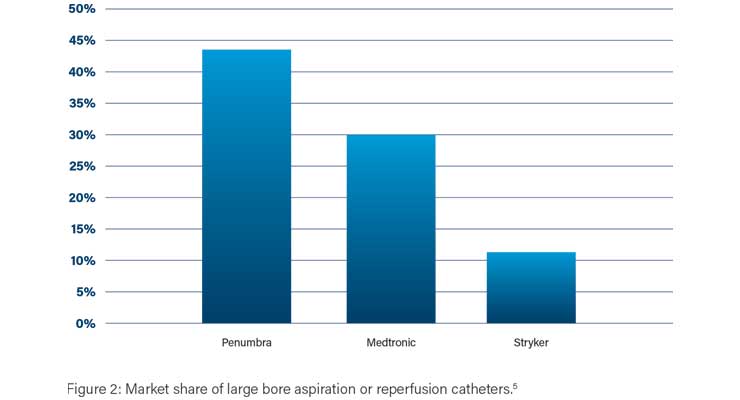

The BTIG survey gets very specific about catheter design. When asked, “Of your procedures done with a direct aspiration first-pass technique, what percentage use large-bore aspiration catheters or reperfusion catheters from the following companies?” respondents listed the top three were Penumbra, Medtronic, and Stryker (Figure 2).

Figure 2: Market share of large bore aspiration or reperfusion catheters.5

BTIG also queried respondents about ADAPT procedures performed using an aspiration pump. They responded the most frequently used aspiration pump was from Penumbra (40 percent), followed by Medtronic (28 percent) and Stryker (18 percent). The BTIG analysts noted that while Penumbra’s catheter share of ADAPT procedures grew to 44 percent, their aspiration pump share of ADAPT procedures fell to 40 percent from 56 percent.5

The Medi-Vantage Perspective

This is a highly competitive, bare-knuckles fight in the vascular and neurovascular thrombectomy domains and one place to look for a foot in the door is where a market leader has recently lost a significant amount of market share such as Penumbra’s loss of aspiration pump share of ADAPT. The BTIG report does not mention the reasons behind this loss, and the loss of share may not be material. However, there are many up-and-coming start-ups with new technology such as Imperative Care or Rapid Medical that are hungry for market share and will be examining every strategic opportunity they can find. If you are Penumbra, you should be finding ways to raise the drawbridge; if you are a competitor, you should be looking for ways to cross the moat. It is all about strategy.

References

Maria Shepherd has more than 20 years of leadership experience in medical device/life-science marketing in small startups and top-tier companies. After her industry career, including her role as vice president of marketing for Oridion Medical, where she boosted the company valuation prior to its acquisition by Medtronic, director of marketing for Philips Medical, and senior management roles at Boston Scientific Corp., she founded Medi-Vantage. Medi-Vantage provides marketing and business strategy and innovation research for the medical device industry. The firm quantitatively and qualitatively sizes and segments opportunities, evaluates new technologies, provides marketing services, and assesses prospective acquisitions. Shepherd has taught marketing and product development courses, speaks regularly at medtech conferences, and can be reached at mshepherd@medi-vantage.com. Visit her website at www.medi-vantage.com.

Why This Is Important

There are other options, however, to treat these conditions. According to Inari executive leadership speaking at the SVB Leerink conference,2 the VTE markets for DVT and pulmonary embolism (PE) treatment can also be treated by mechanical thrombectomy. They believe the markets for DVT and PE remain deeply underpenetrated by VTE interventional technology with approximately 10 percent of PE patients, and a slightly greater percentage of DVT patients, being treated interventionally with mechanical thrombectomy. Analysts from SVBLeerink believe this indicates a large runway remains ahead of Inari and their competitors as they continue to penetrate these markets.2

Interventions in Peripheral Vascular Disease

Also in the peripheral vascular segment, Penumbra—a direct competitor of Inari—reported the U.S. vascular thrombectomy segment growing by 10 percent.3 While Penumbra reported procedural declines from increased rates of COVID-related VTE since the onset, executive management stated this factor doesn’t appear to be significantly affecting their numbers to date. Market development continues to expand technology utilization into a broader range of patients within the venous segment, especially for those traditionally given conservative medical management. Patients with peripheral artery disease (PAD) are at risk for cardiovascular and limb ischemic events, including acute limb ischemia (ALI).4 ALI is characterized by the sudden decrease in limb perfusion that threatens viability of the limb.

Penumbra management indicates that recently launched technology—the Lightning 7 (designed for single session arterial thrombus removal)—has been well received by interventionalists.

Interventions in Neurovascular Disease

Stroke mechanical thrombectomy (SMT) is another large market for thrombectomy devices. In a BTIG 3rd annual survey of the neurovascular device space, SMT adoption saw a slowdown in 2020 due to COVID, but since then, SMT use has grown steadily.5 In the BTIG 2021 survey, they estimated SMT adoption was growing from 2019 through 2021 at a CAGR of ~16 percent, and CAGR would increase to ~17 percent through 2025. BTIG also estimates the serviceable addressable market of ischemic strokes is ~200,000 annually in the U.S., and estimated market share of SMT is ~25 percent. This survey yields interesting results. The field of interventional neurology continues to grow, with 92 percent of interventional neurologists reporting they treat stroke patients versus eight percent of interventional neuroradiologists.

These numbers are important. Several interventionalists in this survey mentioned the increased use of perfusion imaging as a new tool in treating stroke patients. Perfusion imaging uses an intravascular tracer and serial imaging to measure blood flow in the brain.6 In acute ischemic stroke, perfusion imaging may improve diagnostic accuracy, aid treatment target identification, and provide information about functional outcome. In addition, perfusion imaging can recognize which patients may benefit from reperfusion outside the conventional time window or those where the time of symptom onset is unknown.

Using perfusion imaging in the treatment of acute stroke allows personalized treatment of stroke patients based on the condition of their brain tissue, as opposed to traditional time-based treatment.

The BTIG survey also estimated stent retriever share was highest for Medtronic, followed by Penumbra and Stryker (Figure 1).5 A new company rapidly gaining market share is Rapid Medical, a private company that launched the Tigertriever in the U.S. in 2Q21. BTIG analysts believe there could be growing use of stent retrievers for deep clots in the brain where the opportunity for aspiration may be restricted.

When asked what percent of your ischemic stroke patients do you treat with SMT (defined as stent retrievers, coil retrievers, or aspiration catheters) and if that percentage of patients treated with SMT will increase or decrease in the next 12 months, respondents signaled an increase in use of SMT from 25 percent in Feb 2022 to 29 percent in February of 2023. When asked about treatment of stroke patients using an SMT direct aspiration first-pass technique (ADAPT), physicians responded that using these types of catheters will increase to 37 percent of all SMT procedures by May 2022 and was expected to further increase to 40 percent of all SMT used. Reasons given were that these catheters were successful 80 percent of the time in removing clots, and this technology was a substantial improvement.5

Respondents are also willing to combine devices if they expect it will improve outcomes. Use of a stent retriever in combination with an aspiration device is a technique called “Solumbra.”7 It has emerged as a popular method of mechanical thrombectomy for acute ischemic stroke. There are multiple variations in the technique, few have been studied, and it is uncertain how these techniques affect patient outcomes. The BTIG respondents estimated the percent of SMT patients treated using Solumbra will rise to 13.9 percent to 14.3 percent.5

The BTIG survey gets very specific about catheter design. When asked, “Of your procedures done with a direct aspiration first-pass technique, what percentage use large-bore aspiration catheters or reperfusion catheters from the following companies?” respondents listed the top three were Penumbra, Medtronic, and Stryker (Figure 2).

Figure 2: Market share of large bore aspiration or reperfusion catheters.5

BTIG also queried respondents about ADAPT procedures performed using an aspiration pump. They responded the most frequently used aspiration pump was from Penumbra (40 percent), followed by Medtronic (28 percent) and Stryker (18 percent). The BTIG analysts noted that while Penumbra’s catheter share of ADAPT procedures grew to 44 percent, their aspiration pump share of ADAPT procedures fell to 40 percent from 56 percent.5

The Medi-Vantage Perspective

This is a highly competitive, bare-knuckles fight in the vascular and neurovascular thrombectomy domains and one place to look for a foot in the door is where a market leader has recently lost a significant amount of market share such as Penumbra’s loss of aspiration pump share of ADAPT. The BTIG report does not mention the reasons behind this loss, and the loss of share may not be material. However, there are many up-and-coming start-ups with new technology such as Imperative Care or Rapid Medical that are hungry for market share and will be examining every strategic opportunity they can find. If you are Penumbra, you should be finding ways to raise the drawbridge; if you are a competitor, you should be looking for ways to cross the moat. It is all about strategy.

References

- bit.ly/mpo220401

- bit.ly/mpo220402

- Truist analyst report 11/24/21 Lightning of Growth: Q3 Beats, Led by Expansion in Vascular & Resurgence in US Neuro Thrombectomy

- bit.ly/mpo220404

- bit.ly/mpo220405

- bit.ly/mpo220406

- bit.ly/mpo220407

Maria Shepherd has more than 20 years of leadership experience in medical device/life-science marketing in small startups and top-tier companies. After her industry career, including her role as vice president of marketing for Oridion Medical, where she boosted the company valuation prior to its acquisition by Medtronic, director of marketing for Philips Medical, and senior management roles at Boston Scientific Corp., she founded Medi-Vantage. Medi-Vantage provides marketing and business strategy and innovation research for the medical device industry. The firm quantitatively and qualitatively sizes and segments opportunities, evaluates new technologies, provides marketing services, and assesses prospective acquisitions. Shepherd has taught marketing and product development courses, speaks regularly at medtech conferences, and can be reached at mshepherd@medi-vantage.com. Visit her website at www.medi-vantage.com.