Christopher J. Calhoun, Chairman and CEO, Paracrine Inc.02.07.22

Innovative biotechnology companies potentially can transform healthcare, developing new therapies that may improve and extend patients’ lives. Delivering on this promise is an epic journey that may take one to two decades, unimaginable amounts of cash, and surviving the notorious “valley of death.”

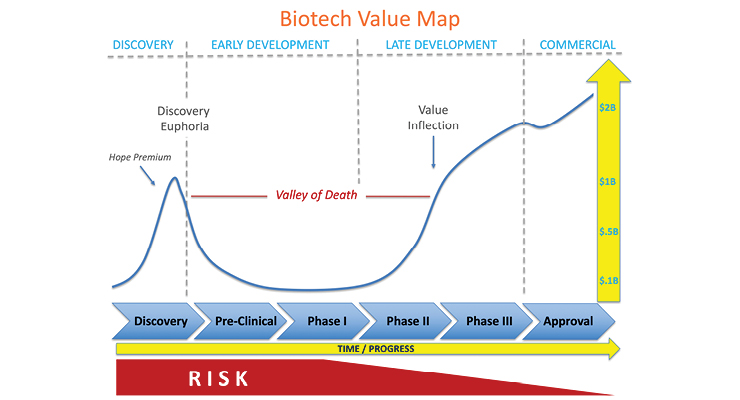

Discovery Euphoria

Innovation begins with a discovery typically emanating from grant-funded research in academia. The startup is born and often supported through seed funding from friends and family. The sexiest technologies that elicit exciting promises of new scientific frontiers (think genome editing tool CRISPR) or the next silver bullet that may cure a specific disease (like CAR T-cell therapy engineered for a specific type of cancer) can shoot these new company valuations into the stratosphere. Venture investors compete to find the next unicorn (companies with a valuation of more than $1 billion) and are willing to place smart bets on the most promising discoveries. Despite the fact that these early biotechnologies are unproven with virtually no clinical data, company valuations soar because they are fueled by a “hope premium” characteristic to the promise driving Discovery Euphoria.

The ‘Hope Premium’

The initial surge of funding for biotechnologies arrives at the beginning—the discovery stage. At this point, the therapy is still at the benchtop—no animal testing or human studies have been conducted to prove its effectiveness; therefore no safety issues have come to light. Investors at this stage are trading on a “hope premium” that’s based solely on the idea of the product’s potential, as they have no concrete proof of its safety or effectiveness. Companies may raise tens of millions of dollars and recently, even hundreds of millions of dollars at this stage without treating a single patient. However, difficult times are just around the corner.

The ‘Valley of Death’

Discovery euphoria quickly fades as the company quietly transitions from benchtop to pre-clinical (animal) research. Utilizing its new pile of capital, the company expands by adding people, facilities, and often new targets or technology into the pipeline. Advancing through pre-clinical studies and then human clinical trials is the major focus at this stage. This early development period is abundant with risk across all fronts that may threaten the feasibility of the technology and even the company’s viability.

The cash begins to flow, or rather flow out. Losses accumulate and the amount of cash in the bank evaporates—a process commonly referred to as the burn rate. There is a constant race to achieve meaningful milestones that reduce the technological risk and demonstrate progress so the company can access more essential capital and move forward before the cash runs out. This iterative cycle may continue for five to 10 years, leading to investor fatigue, shareholder dilution, and an increasing cost of capital, as valuations can languish while traversing the valley of death and potentially fall victim to the unexpected landmines that can threaten their survival. Countless carcasses scatter the landscape across the valley of death; few have survived the gauntlet.

Value Inflection Point

Success in early human safety studies, also known as Phase I or Phase I/IIa trials, may provide a new source of tailwind to push forward, but typically this is not enough to elevate depressed valuations because significant risks remain with larger, longer, more expensive trials still to come. The majority of investors and strategic partners wait for results from the next step—Phase II/IIB clinical trials—before committing significant capital.

Positive Phase II/IIB clinical trial data triggers a value inflection point that may benefit from two parallel forces. First, the investor base may expand to include a large new class of institutional investors that invest in late-stage biotech companies. Increasing demand for and higher trading volume of company stock will increase share price as new investors build a position in the company. Second, large strategic players are always on the hunt for promising products to add to their portfolio. Typically, strategics look for positive Phase II/IIB data as the entry point for partnership or acquisition, as the risk profile has been substantially reduced. With a limited number of viable technologies touting robust Phase II/IIB data, competition may be intense for high-quality product candidates, further driving up value.

Late-Stage Development and Market Entry

Now that the company has successfully navigated the valley of death, management can focus on late-stage trials and prepare for commercialization. The company should be well-positioned to secure additional capital or a strategic partner to advance through the final clinical trials to market approval and deliver on its promise to both patients and shareholders.

Christopher J. Calhoun is Chairman and CEO of Paracrine Inc., a biotechnology company developing the world’s first autologous, device-based disease modifying cell therapy for chronic conditions into late (approval) stage clinical trials based on robust prior clinical data. Calhoun also has served as chief executive of Hi Tech Honeycomb, Integrated Healthcare Alliance, and Cytori Therapeutics. Calhoun is the co-inventor on multiple U.S. and international patents for medical devices and implant instrumentation. He was also involved in research and management for the Plastic Surgery Bone Histology and Histometry Laboratory at the University of California, San Diego. Calhoun is a co-founder and board chairman of Leonardo MD, and has previously served on the StemSource Inc. board.

Discovery Euphoria

Innovation begins with a discovery typically emanating from grant-funded research in academia. The startup is born and often supported through seed funding from friends and family. The sexiest technologies that elicit exciting promises of new scientific frontiers (think genome editing tool CRISPR) or the next silver bullet that may cure a specific disease (like CAR T-cell therapy engineered for a specific type of cancer) can shoot these new company valuations into the stratosphere. Venture investors compete to find the next unicorn (companies with a valuation of more than $1 billion) and are willing to place smart bets on the most promising discoveries. Despite the fact that these early biotechnologies are unproven with virtually no clinical data, company valuations soar because they are fueled by a “hope premium” characteristic to the promise driving Discovery Euphoria.

The ‘Hope Premium’

The initial surge of funding for biotechnologies arrives at the beginning—the discovery stage. At this point, the therapy is still at the benchtop—no animal testing or human studies have been conducted to prove its effectiveness; therefore no safety issues have come to light. Investors at this stage are trading on a “hope premium” that’s based solely on the idea of the product’s potential, as they have no concrete proof of its safety or effectiveness. Companies may raise tens of millions of dollars and recently, even hundreds of millions of dollars at this stage without treating a single patient. However, difficult times are just around the corner.

The ‘Valley of Death’

Discovery euphoria quickly fades as the company quietly transitions from benchtop to pre-clinical (animal) research. Utilizing its new pile of capital, the company expands by adding people, facilities, and often new targets or technology into the pipeline. Advancing through pre-clinical studies and then human clinical trials is the major focus at this stage. This early development period is abundant with risk across all fronts that may threaten the feasibility of the technology and even the company’s viability.

The cash begins to flow, or rather flow out. Losses accumulate and the amount of cash in the bank evaporates—a process commonly referred to as the burn rate. There is a constant race to achieve meaningful milestones that reduce the technological risk and demonstrate progress so the company can access more essential capital and move forward before the cash runs out. This iterative cycle may continue for five to 10 years, leading to investor fatigue, shareholder dilution, and an increasing cost of capital, as valuations can languish while traversing the valley of death and potentially fall victim to the unexpected landmines that can threaten their survival. Countless carcasses scatter the landscape across the valley of death; few have survived the gauntlet.

Value Inflection Point

Success in early human safety studies, also known as Phase I or Phase I/IIa trials, may provide a new source of tailwind to push forward, but typically this is not enough to elevate depressed valuations because significant risks remain with larger, longer, more expensive trials still to come. The majority of investors and strategic partners wait for results from the next step—Phase II/IIB clinical trials—before committing significant capital.

Positive Phase II/IIB clinical trial data triggers a value inflection point that may benefit from two parallel forces. First, the investor base may expand to include a large new class of institutional investors that invest in late-stage biotech companies. Increasing demand for and higher trading volume of company stock will increase share price as new investors build a position in the company. Second, large strategic players are always on the hunt for promising products to add to their portfolio. Typically, strategics look for positive Phase II/IIB data as the entry point for partnership or acquisition, as the risk profile has been substantially reduced. With a limited number of viable technologies touting robust Phase II/IIB data, competition may be intense for high-quality product candidates, further driving up value.

Late-Stage Development and Market Entry

Now that the company has successfully navigated the valley of death, management can focus on late-stage trials and prepare for commercialization. The company should be well-positioned to secure additional capital or a strategic partner to advance through the final clinical trials to market approval and deliver on its promise to both patients and shareholders.

Christopher J. Calhoun is Chairman and CEO of Paracrine Inc., a biotechnology company developing the world’s first autologous, device-based disease modifying cell therapy for chronic conditions into late (approval) stage clinical trials based on robust prior clinical data. Calhoun also has served as chief executive of Hi Tech Honeycomb, Integrated Healthcare Alliance, and Cytori Therapeutics. Calhoun is the co-inventor on multiple U.S. and international patents for medical devices and implant instrumentation. He was also involved in research and management for the Plastic Surgery Bone Histology and Histometry Laboratory at the University of California, San Diego. Calhoun is a co-founder and board chairman of Leonardo MD, and has previously served on the StemSource Inc. board.