Kristin Pothier and Anuj Kapadia, KPMG05.01.20

Fifty-eight percent of respondents to KPMG’s 2020 Healthcare and Life Sciences Investment Outlook expect to see an increase in deal volume this year compared to 2019. Investment activity will continue to be triggered by portfolio and market expansion, scale and synergy plays (including horizontal and vertical acquisitions), and building new capabilities, especially in technology.

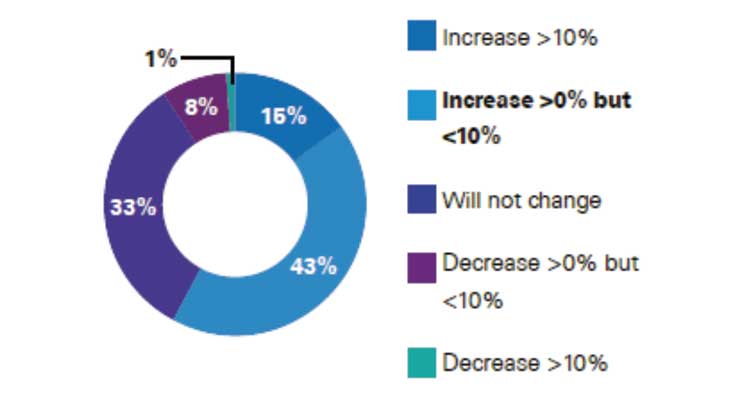

Approximately 44 percent of respondents among corporate finance executives also believe there are moderate to strong fundamentals driving the life sciences sector (see chart). While factors such as the COVID-19 outbreak will likely prompt additional investment considerations, other disruptors such as new innovations and new entrants including technology players are expected to increase overall M&A activity this year.

There has been robust innovation in the medical devices and diagnostics sector. Advances in robotic surgery are transforming routine and non-routine procedures—this market has already attracted major M&A interest, with buyers investing more than $6 billion in new platforms. And device makers are seeking innovative products for these platforms, e.g. Johnson & Johnson acquired Auris Health Inc. to gain access to the Monarch robotic diagnostics platform, which can be used to perform lung biopsies and is expected to be approved for cancer surgeries in the future. Other innovations include robot cameras that physicians can control with eye movements and a GPS-like map that can be projected onto a patient’s body before surgery.

Precision medicine links diagnostics and therapeutics and continues to be a major focus area, as evidenced by the acquisition of Brammer Bio by Thermo-Fisher Scientific Inc. for $1.7 billion to increase its presence in cell and gene therapies. In early March, Thermo Fisher also bought Qiagen NV for $11.5 billion; the combined company will accelerate the development of higher-specificity, faster, and more comprehensive tests that can improve patient outcomes and reduce the overall cost of care.

Smart wearables are facilitating detailed patient tracking and artificial intelligence (AI) is transforming healthcare, offering the potential for better personalization, improved clinical decision-making, predictive analytics, and chronic disease management to lower costs. The U.S. Food and Drug Administration has already approved a number of medical devices driven by AI software, including one that can detect diabetic retinopathy and one that can alert providers to the likelihood that a patient will suffer a stroke. AI is also rapidly advancing the imaging sector, fueling new equipment and enabling existing equipment to be smarter, faster, and more reliable.

The shift to value and convergence along the healthcare value chain are other emerging trends impacting the future for the medical device and diagnostics sector.

With a clear shift from cost to value in the healthcare industry, medical device manufacturers need to integrate value-added offerings into their portfolio. They can do this by investing in a digital and technology backbone that links data to the device for consistently defined outcomes and increased transparency across healthcare stakeholders. Additionally, companies need to adopt a ‘user-back’ approach instead of the traditional ‘device forward’ one, as smart devices are increasingly being used outside the hospital in lower cost and more convenient care settings, including at home.

Driven by the need to provide quality care at lower costs, the sector will see continued entry of new players from all industries, especially disruptive technology companies. For example, Google’s Project Nightingale is using advanced AI and machine learning to suggest targeted changes in patient care to improve outcomes. Although initiatives like this have raised data privacy concerns, medical device companies are increasingly forging partnerships with technology players.

Medical device companies are also increasingly focusing on convergence with other sectors, which is leading to the creation of complementary services and offerings for certain disease areas, such as diabetes—Dexcom Inc. has collaborated with the Apple Watch, allowing patients to see their continuous glucose monitoring information on their wrist. Diagnostics companies are also working with pharmaceutical players to provide full patient customization. For example, Loxo Oncology Inc. partnered with Illumina Inc. to develop tests that determine patient eligibility for Loxo’s cancer drugs, across tumor types.

Fueled by all these developments, there is significant potential in the following three focus areas for investors in the medical device and diagnostics sector:

While companies continue to keep a close eye on the changing regulatory landscape (e.g., EU MDR, IVDR, etc.), there are clear inorganic growth opportunities for medical device and diagnostics investors in 2020.

Kristin Pothier leads KPMG’s Healthcare & Life Sciences sector for the Deal Advisory and Strategy practice. Kristin’s product and service launch experience includes more than 20 years of strategy and operations in scientific, clinical, and OTC/ DTC markets.

Anuj Kapadia is a director at KPMG’s Strategy practice, where he has worked across the healthcare and life sciences value chain, including corporate strategy formulation, M&A, operational excellence programs, sales and marketing strategies, outsourcing, and regulatory compliance.

Approximately 44 percent of respondents among corporate finance executives also believe there are moderate to strong fundamentals driving the life sciences sector (see chart). While factors such as the COVID-19 outbreak will likely prompt additional investment considerations, other disruptors such as new innovations and new entrants including technology players are expected to increase overall M&A activity this year.

There has been robust innovation in the medical devices and diagnostics sector. Advances in robotic surgery are transforming routine and non-routine procedures—this market has already attracted major M&A interest, with buyers investing more than $6 billion in new platforms. And device makers are seeking innovative products for these platforms, e.g. Johnson & Johnson acquired Auris Health Inc. to gain access to the Monarch robotic diagnostics platform, which can be used to perform lung biopsies and is expected to be approved for cancer surgeries in the future. Other innovations include robot cameras that physicians can control with eye movements and a GPS-like map that can be projected onto a patient’s body before surgery.

Precision medicine links diagnostics and therapeutics and continues to be a major focus area, as evidenced by the acquisition of Brammer Bio by Thermo-Fisher Scientific Inc. for $1.7 billion to increase its presence in cell and gene therapies. In early March, Thermo Fisher also bought Qiagen NV for $11.5 billion; the combined company will accelerate the development of higher-specificity, faster, and more comprehensive tests that can improve patient outcomes and reduce the overall cost of care.

Smart wearables are facilitating detailed patient tracking and artificial intelligence (AI) is transforming healthcare, offering the potential for better personalization, improved clinical decision-making, predictive analytics, and chronic disease management to lower costs. The U.S. Food and Drug Administration has already approved a number of medical devices driven by AI software, including one that can detect diabetic retinopathy and one that can alert providers to the likelihood that a patient will suffer a stroke. AI is also rapidly advancing the imaging sector, fueling new equipment and enabling existing equipment to be smarter, faster, and more reliable.

The shift to value and convergence along the healthcare value chain are other emerging trends impacting the future for the medical device and diagnostics sector.

With a clear shift from cost to value in the healthcare industry, medical device manufacturers need to integrate value-added offerings into their portfolio. They can do this by investing in a digital and technology backbone that links data to the device for consistently defined outcomes and increased transparency across healthcare stakeholders. Additionally, companies need to adopt a ‘user-back’ approach instead of the traditional ‘device forward’ one, as smart devices are increasingly being used outside the hospital in lower cost and more convenient care settings, including at home.

Driven by the need to provide quality care at lower costs, the sector will see continued entry of new players from all industries, especially disruptive technology companies. For example, Google’s Project Nightingale is using advanced AI and machine learning to suggest targeted changes in patient care to improve outcomes. Although initiatives like this have raised data privacy concerns, medical device companies are increasingly forging partnerships with technology players.

Medical device companies are also increasingly focusing on convergence with other sectors, which is leading to the creation of complementary services and offerings for certain disease areas, such as diabetes—Dexcom Inc. has collaborated with the Apple Watch, allowing patients to see their continuous glucose monitoring information on their wrist. Diagnostics companies are also working with pharmaceutical players to provide full patient customization. For example, Loxo Oncology Inc. partnered with Illumina Inc. to develop tests that determine patient eligibility for Loxo’s cancer drugs, across tumor types.

Fueled by all these developments, there is significant potential in the following three focus areas for investors in the medical device and diagnostics sector:

- Robotic surgery: In the more classic medical device segment, robotic surgery will continue to attract interest (notwithstanding Medtronic plc’s recent safety issues with the Mazor platform)

- Non-invasive diagnostics options: Precision medicine will continue to drive growth and M&A in the diagnostics segment, through new and innovative minimally invasive technologies

- AI-enabled devices: In the race to deliver secure, data-driven and value-based care, smart devices powered by AI will lead to various industry deals and partnerships

While companies continue to keep a close eye on the changing regulatory landscape (e.g., EU MDR, IVDR, etc.), there are clear inorganic growth opportunities for medical device and diagnostics investors in 2020.

Kristin Pothier leads KPMG’s Healthcare & Life Sciences sector for the Deal Advisory and Strategy practice. Kristin’s product and service launch experience includes more than 20 years of strategy and operations in scientific, clinical, and OTC/ DTC markets.

Anuj Kapadia is a director at KPMG’s Strategy practice, where he has worked across the healthcare and life sciences value chain, including corporate strategy formulation, M&A, operational excellence programs, sales and marketing strategies, outsourcing, and regulatory compliance.