08.02.10

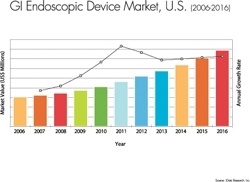

The market for anti-reflux devices more than tripled last year, easily bypassing the second fastest-growing segment, capsule endoscopic devices, according a report by iData Inc. Titled “U.S. Market for Gastrointestinal Endoscopic Devices,” the report covers the decade spanning 2006-2016.

It forecasts an annual growth rate increase of 67 percent, with a spike in 2011 due to robust sales as products are more readily adopted.

GI endoscopes are expected to maintain the market lead throughout the forecast period. Market growth for GI endoscopes is mostly fueled by the demand for colonoscopes, which represent more than 50 percent of the GI endoscopic device market. Although colonoscopes will remain the largest segment, the fastest growing segments in the market for GI endoscopes will be transnasal products and double-balloon devices. These segments are expected to nearly quadruple their value by the end of 2016, and the ultrasound endoscope market is expected to nearly triple in value, according to the report.

Capsule endoscopic devices was the second-fastest growing gastrointestinal endoscopic device segment in 2009 due to technological advancements in both the camera capsule and data recorders sectors. Volumes are expected to surpass 1.5 million by 2016, and market value also is expected to increase substantially over the forecast period. Advancements in image quality and the increased image capture rate of camera capsules has fueled the market, as has the introduction of wireless data recorders, which provide increased patient comfort and eliminate the need for patient preparation, according to the report.

Foreign body removal devices represented the smallest segment in the U.S. market in 2009 for GI endoscopy. This market is expected to continue to decline over the forecast period because product innovation will be minimal, the report said.

In 2009, more than 55 million procedures were performed with GI endoscopic devices, and nearly 50 percent of those procedures were colonoscopies. The numbers reflect the growing frequency of regular colon exams for early diagnosis of colorectal cancer.

The GI endoscopic market includes GI endoscopes, capsule endoscopic devices, virtual colonoscopy software, stenting devices, dilation balloons, endoscopic retrograde cholangiopancreatography (ERCP) devices, biopsy forceps, polypectomy snares, fine aspiration needles, specimen and foreign body retrieval devices, hemostasis devices, anti-reflux devices and enteral feeding.

It forecasts an annual growth rate increase of 67 percent, with a spike in 2011 due to robust sales as products are more readily adopted.

GI endoscopes are expected to maintain the market lead throughout the forecast period. Market growth for GI endoscopes is mostly fueled by the demand for colonoscopes, which represent more than 50 percent of the GI endoscopic device market. Although colonoscopes will remain the largest segment, the fastest growing segments in the market for GI endoscopes will be transnasal products and double-balloon devices. These segments are expected to nearly quadruple their value by the end of 2016, and the ultrasound endoscope market is expected to nearly triple in value, according to the report.

Capsule endoscopic devices was the second-fastest growing gastrointestinal endoscopic device segment in 2009 due to technological advancements in both the camera capsule and data recorders sectors. Volumes are expected to surpass 1.5 million by 2016, and market value also is expected to increase substantially over the forecast period. Advancements in image quality and the increased image capture rate of camera capsules has fueled the market, as has the introduction of wireless data recorders, which provide increased patient comfort and eliminate the need for patient preparation, according to the report.

Foreign body removal devices represented the smallest segment in the U.S. market in 2009 for GI endoscopy. This market is expected to continue to decline over the forecast period because product innovation will be minimal, the report said.

In 2009, more than 55 million procedures were performed with GI endoscopic devices, and nearly 50 percent of those procedures were colonoscopies. The numbers reflect the growing frequency of regular colon exams for early diagnosis of colorectal cancer.

The GI endoscopic market includes GI endoscopes, capsule endoscopic devices, virtual colonoscopy software, stenting devices, dilation balloons, endoscopic retrograde cholangiopancreatography (ERCP) devices, biopsy forceps, polypectomy snares, fine aspiration needles, specimen and foreign body retrieval devices, hemostasis devices, anti-reflux devices and enteral feeding.