Mihir Torsekar, Analyst, U.S. International Trade Commission01.29.20

As we start a new decade, I thought it would be a good time to review and reflect on some key industry trends I observed over the past 10 years. This column covers the trade story, the rise of non-tariff measures (NTMs), the expansion of technology into medtech supply chains, and the emergence of the East Asia-Pacific region as a major player in global medtech supply chains. I’ll also share some of the big questions on my mind as we enter a new year (and decade).

Trade Story

In the decades preceding the 2010s, medtech supply chains were highly fragmented. This was largely the result of Western multinationals outsourcing and offshoring parts and components manufacturing to countries with low-labor costs, while specializing in high-value added activities (i.e., research and development, marketing, and logistics). In addition to financial incentives provided by the host countries, this supply chain strategy owed largely to free trade agreements, which granted duty-free access for multinationals. This translated into a high volume of medtech trade, led by parts.

During this period, global medtech trade expanded by over 200 percent, while parts trade alone grew by 330 percent. For the most part, the trend toward trade liberalization continued throughout the 2010s. The U.S.-Korea Trade Agreement took effect in 2012, while the implementation of the U.S.-Mexico-Canada Agreement (USMCA) appears imminent. Both trade agreements included specific annexes covering medical devices as well as chapters benefitting the sector, such as customs and trade facilitation and technical barriers to trade. In the case of the USMCA, chapters cover subject matter ranging from digital trade, good regulatory practices, and secure commitments from North American trading partners to maintaining open cross-border data flows and adopting best international regulatory practices.

Outside of the United States, the Association of Southeast Asian Nations (ASEAN), a regional intergovernmental organization of 10 Southeast Asian countries, minted free trade agreements with Australia, New Zealand, and India in 2010. More recently, the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) enjoined 11 countries that collectively accounted for roughly 20 percent of global medtech trade in 2018. Much like the previous trade agreements discussed previously, the CPTPP also included specific chapters that targeted regulatory convergence for the medtech sector. These are certainly promising developments for the sector, as regulatory divergence is a principal impediment to greater market access.

Yet, even while the general trend toward liberalization occurred, the end of the decade saw a greater inclination toward tariffs, highlighted by the U.S.-China trade dispute. At press time, tariffs impacted roughly one-quarter of U.S. medtech-related imports from China.

The Rise of NTMs

Notably, while tariffs have received a substantial amount of attention over the past two years, the steady growth of NTMs may have been more impactful on trade flows during the previous decade. NTMs refer to policy measures (other than customs tariffs) that can potentially have an economic effect on international trade in goods. The measures most relevant to the medtech sector are considered technical in nature and include conformity assessment procedures (i.e., certification, testing, and quality system requirements) and technical regulations (i.e., specifications of product characteristics, labeling requirements, production processes, and testing).

During the past decade, 376 medtech-specific NTMs were implemented worldwide. This stands in sharp contrast to the 145 that entered into force in the decade preceding the 2010s. Notably, NTMs can serve legitimate purposes by ensuring consumer protections and aligning the medtech standards of a particular country with that of international best practices. For example, measures that adopt standards endorsed by the International Medical Device Regulators Forum—such as a risk-based classification system for medical devices—would likely prove trade facilitating. However, NTMs can also be employed to protect domestic industries from import competition, thereby reducing trade. An example could be country-specific labeling requirements or unnecessarily complicated procedures.

Many industry experts with whom I’ve spoken suggest the growth of NTMs is an encouraging trend. In part, it reflects the growing awareness of countries to abide by their commitments under the World Trade Organization’s Technical Barriers to Trade Agreement to notify other members of their intentions to adopt regulatory measures that could substantially influence trade flows.

The Digitalization of Medtech Supply Chains

Throughout the 2010s, the shift toward value-driven healthcare accelerated. During this time, digital technologies (e.g., artificial intelligence, additive manufacturing, and the Internet of Things) abetted by advancements in computing and processing capabilities were increasingly leveraged in the production of medtech. The increasing digitization of medtech supply chains arrived amid a climate of increasing pricing pressures on manufacturers; rising compliance costs owing to stricter regulations in key markets, such as the EU; and operational complexities arising from the spate of industry-wide mergers and acquisitions.

At the same time, the leading “big tech” companies in the United States including Apple, Microsoft, and Alphabet (Google’s parent company) entered into the healthcare space, concentrating on different segments of the sector. For example, Apple has emphasized its consumer products; the iWatch series 4 received U.S. Food and Drug Administration approval as a Class II medical device in 2018. Although tech companies have long provided services to the healthcare industry, the close of the decade found these companies creating or investing in technologies for doctors, patients, and consumers.

The growing involvement of technology in medtech supply chains may also be responsible for elevating concerns other than labor costs as a guide to influencing investment decisions. For example, the application of 3D printing to products such as hearing aids could translate into more regional supply chains, as manufacturers prioritize rapid time-to-market over low-cost labor. Further, the growth of automation during the past decade may also reduce the reliance of medtech manufacturers on low-cost labor, permitting specialization in high-value added activities going forward.

Asia-Pacific’s Rise

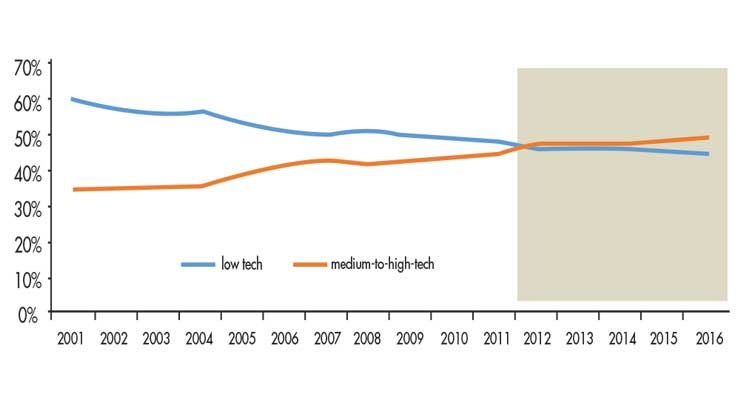

The 2010s witnessed the emergence of the Asia-Pacific region as a critical player in the international medtech supply chain. China was the principal driver of this trend. In the early part of the decade, the country was still a predominant supplier of low-tech goods, but over the past eight years or so, the country transitioned into a viable exporter of higher-tech medical devices (Figure 1). This trend occurred alongside China’s stated intentions under the “Make in China 2025” industrial policy to become more self-sufficient in supplying the country’s advanced medtech market with domestic production.

Figure 1: The share of China’s medtech exports that were low-tech and medium- to high-tech, 2001–16. Source: Torsekar, “China’s Changing Medical Device Exports,” January 2018.

To fulfill this objective, China has increasingly retained its domestic production, rather than exporting it to other countries for final assembly. Having long served as a principal manufacturer and exporter of low-cost goods, this development may explain why the 2010s witnessed a 177 percentage point reduction in the rate of global medtech trade growth relative to the preceding decade.

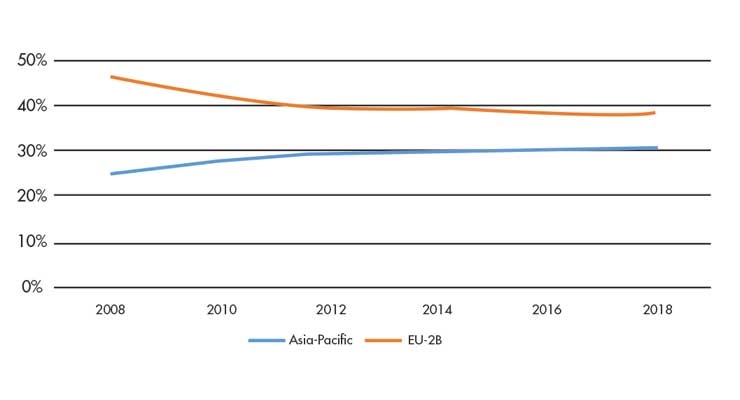

At the same time, China’s ascension into higher segments of the global value chain coupled with rising wages within the country have created opportunities for other regional countries such as Malaysia, Singapore, Thailand, and Vietnam to supply key medtech markets. For example, the region appeared to partially displace the EU as the United States’ leading medtech trading bloc throughout the decade (Figure 2).

Figure 2: Share of total medtech trade between the U.S., the Asia-Pacific region, and the EU-28, 2008–18 Source: Global Trade Atlas.

Much like China, these countries represent chronically underserved medtech markets, which has presented U.S. firms with significant market opportunities. As previously stated, the participation of many of these countries in large trading agreements such as the CPTPP, may facilitate greater medtech trade in the region, as these agreements promise to achieve greater regulatory harmonization.

Conclusion

While some interesting trends emerged during the last decade, the concluding years have left me with a lot of questions. What are the long-term supply chain implications arising from the U.S-China trade dispute? If China succeeds in supplying its high-end medtech market with domestic production, what will that mean for global medtech trade and for U.S. multinationals that are currently the leading suppliers? With uncertainties surrounding the impact of the EU’s MDR, will the Asia-Pacific region continue to chip into the EU’s status as the United States’ leading medtech trading partner?

I hope to answer these questions in the years ahead.

Mihir Torsekar covers trade and competitiveness issues affecting the U.S. and global medical device industry as part of his duties at the United States International Trade Commission.

Trade Story

In the decades preceding the 2010s, medtech supply chains were highly fragmented. This was largely the result of Western multinationals outsourcing and offshoring parts and components manufacturing to countries with low-labor costs, while specializing in high-value added activities (i.e., research and development, marketing, and logistics). In addition to financial incentives provided by the host countries, this supply chain strategy owed largely to free trade agreements, which granted duty-free access for multinationals. This translated into a high volume of medtech trade, led by parts.

During this period, global medtech trade expanded by over 200 percent, while parts trade alone grew by 330 percent. For the most part, the trend toward trade liberalization continued throughout the 2010s. The U.S.-Korea Trade Agreement took effect in 2012, while the implementation of the U.S.-Mexico-Canada Agreement (USMCA) appears imminent. Both trade agreements included specific annexes covering medical devices as well as chapters benefitting the sector, such as customs and trade facilitation and technical barriers to trade. In the case of the USMCA, chapters cover subject matter ranging from digital trade, good regulatory practices, and secure commitments from North American trading partners to maintaining open cross-border data flows and adopting best international regulatory practices.

Outside of the United States, the Association of Southeast Asian Nations (ASEAN), a regional intergovernmental organization of 10 Southeast Asian countries, minted free trade agreements with Australia, New Zealand, and India in 2010. More recently, the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) enjoined 11 countries that collectively accounted for roughly 20 percent of global medtech trade in 2018. Much like the previous trade agreements discussed previously, the CPTPP also included specific chapters that targeted regulatory convergence for the medtech sector. These are certainly promising developments for the sector, as regulatory divergence is a principal impediment to greater market access.

Yet, even while the general trend toward liberalization occurred, the end of the decade saw a greater inclination toward tariffs, highlighted by the U.S.-China trade dispute. At press time, tariffs impacted roughly one-quarter of U.S. medtech-related imports from China.

The Rise of NTMs

Notably, while tariffs have received a substantial amount of attention over the past two years, the steady growth of NTMs may have been more impactful on trade flows during the previous decade. NTMs refer to policy measures (other than customs tariffs) that can potentially have an economic effect on international trade in goods. The measures most relevant to the medtech sector are considered technical in nature and include conformity assessment procedures (i.e., certification, testing, and quality system requirements) and technical regulations (i.e., specifications of product characteristics, labeling requirements, production processes, and testing).

During the past decade, 376 medtech-specific NTMs were implemented worldwide. This stands in sharp contrast to the 145 that entered into force in the decade preceding the 2010s. Notably, NTMs can serve legitimate purposes by ensuring consumer protections and aligning the medtech standards of a particular country with that of international best practices. For example, measures that adopt standards endorsed by the International Medical Device Regulators Forum—such as a risk-based classification system for medical devices—would likely prove trade facilitating. However, NTMs can also be employed to protect domestic industries from import competition, thereby reducing trade. An example could be country-specific labeling requirements or unnecessarily complicated procedures.

Many industry experts with whom I’ve spoken suggest the growth of NTMs is an encouraging trend. In part, it reflects the growing awareness of countries to abide by their commitments under the World Trade Organization’s Technical Barriers to Trade Agreement to notify other members of their intentions to adopt regulatory measures that could substantially influence trade flows.

The Digitalization of Medtech Supply Chains

Throughout the 2010s, the shift toward value-driven healthcare accelerated. During this time, digital technologies (e.g., artificial intelligence, additive manufacturing, and the Internet of Things) abetted by advancements in computing and processing capabilities were increasingly leveraged in the production of medtech. The increasing digitization of medtech supply chains arrived amid a climate of increasing pricing pressures on manufacturers; rising compliance costs owing to stricter regulations in key markets, such as the EU; and operational complexities arising from the spate of industry-wide mergers and acquisitions.

At the same time, the leading “big tech” companies in the United States including Apple, Microsoft, and Alphabet (Google’s parent company) entered into the healthcare space, concentrating on different segments of the sector. For example, Apple has emphasized its consumer products; the iWatch series 4 received U.S. Food and Drug Administration approval as a Class II medical device in 2018. Although tech companies have long provided services to the healthcare industry, the close of the decade found these companies creating or investing in technologies for doctors, patients, and consumers.

The growing involvement of technology in medtech supply chains may also be responsible for elevating concerns other than labor costs as a guide to influencing investment decisions. For example, the application of 3D printing to products such as hearing aids could translate into more regional supply chains, as manufacturers prioritize rapid time-to-market over low-cost labor. Further, the growth of automation during the past decade may also reduce the reliance of medtech manufacturers on low-cost labor, permitting specialization in high-value added activities going forward.

Asia-Pacific’s Rise

The 2010s witnessed the emergence of the Asia-Pacific region as a critical player in the international medtech supply chain. China was the principal driver of this trend. In the early part of the decade, the country was still a predominant supplier of low-tech goods, but over the past eight years or so, the country transitioned into a viable exporter of higher-tech medical devices (Figure 1). This trend occurred alongside China’s stated intentions under the “Make in China 2025” industrial policy to become more self-sufficient in supplying the country’s advanced medtech market with domestic production.

Figure 1: The share of China’s medtech exports that were low-tech and medium- to high-tech, 2001–16. Source: Torsekar, “China’s Changing Medical Device Exports,” January 2018.

To fulfill this objective, China has increasingly retained its domestic production, rather than exporting it to other countries for final assembly. Having long served as a principal manufacturer and exporter of low-cost goods, this development may explain why the 2010s witnessed a 177 percentage point reduction in the rate of global medtech trade growth relative to the preceding decade.

At the same time, China’s ascension into higher segments of the global value chain coupled with rising wages within the country have created opportunities for other regional countries such as Malaysia, Singapore, Thailand, and Vietnam to supply key medtech markets. For example, the region appeared to partially displace the EU as the United States’ leading medtech trading bloc throughout the decade (Figure 2).

Figure 2: Share of total medtech trade between the U.S., the Asia-Pacific region, and the EU-28, 2008–18 Source: Global Trade Atlas.

Much like China, these countries represent chronically underserved medtech markets, which has presented U.S. firms with significant market opportunities. As previously stated, the participation of many of these countries in large trading agreements such as the CPTPP, may facilitate greater medtech trade in the region, as these agreements promise to achieve greater regulatory harmonization.

Conclusion

While some interesting trends emerged during the last decade, the concluding years have left me with a lot of questions. What are the long-term supply chain implications arising from the U.S-China trade dispute? If China succeeds in supplying its high-end medtech market with domestic production, what will that mean for global medtech trade and for U.S. multinationals that are currently the leading suppliers? With uncertainties surrounding the impact of the EU’s MDR, will the Asia-Pacific region continue to chip into the EU’s status as the United States’ leading medtech trading partner?

I hope to answer these questions in the years ahead.

Mihir Torsekar covers trade and competitiveness issues affecting the U.S. and global medical device industry as part of his duties at the United States International Trade Commission.