03.24.15

The global market value for transcatheter heart valves will expand at an impressive compound annual growth rate (CAGR) of 19.7 percent, from almost $881 million in 2013 to around $3.02 billion by 2020, according to United Kingdom-based research and consulting firm GlobalData.

The firm's analysts report that the rate is almost three times the projected value of the tissue heart valves market, which will increase at a much slower CAGR of 3.2 percent to just under $1.08 billion over the same period.

GlobalData’s forecast only considers aortic valve replacement, as there are not yet any approved transcatheter mitral valve replacement (TMVR) devices. The approval of TMVR devices will have a significant impact on this forecast, analysts noted, "but early adoption rates are expected to be slow due to initial cost," they wrote.

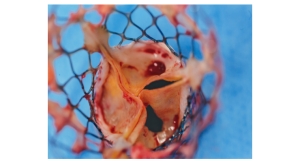

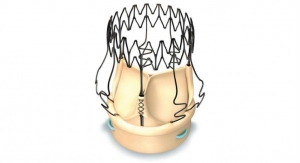

While surgical valves will hold a steady presence in the overall prosthetic valve market, transcatheter aortic valve replacement (TAVR) is expected to cannibalize a large portion of this market in the coming decade. As increasing competition drives down device costs, patients will subsequently have better access to minimally invasive treatment. Current players in the U.S. TAVR market are Irvine, Calif.-based Edwards Lifesciences Corp.; Marlborough, Mass.-based Boston Scientific Corp.; and Dublin, Ireland-based Medtronic plc.

Premdharan Meyyan, GlobalData’s Analyst covering medical devices, says that while first-generation devices have shown promising clinical outcomes to date, physicians have noted issues such as paravalvular regurgitation and a lack of repositionability. These concerns are being addressed in second- and third-generation TAVR devices.

“Transcatheter valves that are fully repositionable and retrievable address some of the main issues inherent in earlier products. Notable devices include Boston Scientific’s Lotus Valve System, Edwards Lifesciences’ Sapien 3, and Medtronic’s CoreValve Evolut R, the latter of which recently displayed a 6.5 percent improvement in all-cause mortality rate compared to open-heart surgery at the two-year mark," said Meyyan. "The adoption of these next-generation valves is expected to drive significant market growth, provided that clinical data continues to show positive mortality and morbidity outcomes for patients.”

Meyyan added that as only high-risk or inoperable aortic valve disease patients are currently eligible for TAVR, more robust, long-term clinical data must be established before the treatment is offered to lower-risk patients.

“Until then, physicians will likely opt for the surgical option, as there is a multitude of clinical data proving efficacy. However, GlobalData believes it is likely that the indications for TAVR will expand and the technology will begin to dominate the surgical market over the forecast period,” Meyyan said.

The firm's analysts report that the rate is almost three times the projected value of the tissue heart valves market, which will increase at a much slower CAGR of 3.2 percent to just under $1.08 billion over the same period.

GlobalData’s forecast only considers aortic valve replacement, as there are not yet any approved transcatheter mitral valve replacement (TMVR) devices. The approval of TMVR devices will have a significant impact on this forecast, analysts noted, "but early adoption rates are expected to be slow due to initial cost," they wrote.

While surgical valves will hold a steady presence in the overall prosthetic valve market, transcatheter aortic valve replacement (TAVR) is expected to cannibalize a large portion of this market in the coming decade. As increasing competition drives down device costs, patients will subsequently have better access to minimally invasive treatment. Current players in the U.S. TAVR market are Irvine, Calif.-based Edwards Lifesciences Corp.; Marlborough, Mass.-based Boston Scientific Corp.; and Dublin, Ireland-based Medtronic plc.

Premdharan Meyyan, GlobalData’s Analyst covering medical devices, says that while first-generation devices have shown promising clinical outcomes to date, physicians have noted issues such as paravalvular regurgitation and a lack of repositionability. These concerns are being addressed in second- and third-generation TAVR devices.

“Transcatheter valves that are fully repositionable and retrievable address some of the main issues inherent in earlier products. Notable devices include Boston Scientific’s Lotus Valve System, Edwards Lifesciences’ Sapien 3, and Medtronic’s CoreValve Evolut R, the latter of which recently displayed a 6.5 percent improvement in all-cause mortality rate compared to open-heart surgery at the two-year mark," said Meyyan. "The adoption of these next-generation valves is expected to drive significant market growth, provided that clinical data continues to show positive mortality and morbidity outcomes for patients.”

Meyyan added that as only high-risk or inoperable aortic valve disease patients are currently eligible for TAVR, more robust, long-term clinical data must be established before the treatment is offered to lower-risk patients.

“Until then, physicians will likely opt for the surgical option, as there is a multitude of clinical data proving efficacy. However, GlobalData believes it is likely that the indications for TAVR will expand and the technology will begin to dominate the surgical market over the forecast period,” Meyyan said.